The European payments market reached about €550 billion in 2025 and is expected to keep expanding at nearly 15% per year through 2031—growth that is largely driven by the ongoing shift from cash to digital payments.

Between 2019 and 2024, online payments grew from 7% to 21% of all transactions, while their share of the total payment value doubled.

For businesses, this shift means one thing: accepting multiple online payment options is no longer optional if you want to stay competitive.

To do so, you’ll usually have to choose between a payment aggregator and a merchant account.

Both allow you to accept card payments and other digital payment methods, which is why they’re often compared.

However, that’s where most similarities end.

The two models take very different approaches to handling payments, managing accounts, and supporting businesses as they grow.

To help you decide which approach is better for your business, this guide gives you a full payment aggregator vs. merchant account breakdown, covering how each model works and what the key differences are.

Key takeaways

- Payment aggregators let businesses start accepting payments quickly

A payment aggregator allows businesses to accept digital payments without opening their own merchant account. You operate under the provider’s shared account, which means faster onboarding, minimal paperwork, and simple payment tools that can get you live within days. - Merchant accounts provide more customization and control

A merchant account is created specifically for one business and includes a unique merchant ID. Because the provider performs detailed underwriting before approval, businesses often get more control over payment settings, payout schedules, and risk management. - The right option depends on your business model and payment needs

There is no universally “better” option. The choice usually depends on factors like transaction volume, industry requirements, growth plans, and how much control you need over your payment setup. - Payment aggregators are ideal for modern, flexible businesses

Aggregators work particularly well for startups, online-first businesses, service providers, and companies testing new concepts. They offer quick setup, ready-to-use integrations, and payment tools that support deposits, bookings, subscriptions, and occasional payments without complex infrastructure. - Paypercut makes payment aggregation simple and scalable

If you want a fast and flexible way to accept payments, Paypercut provides an all-in-one platform with cards, digital wallets, QR payments, and Buy Now, Pay Later options (where available) in one setup. With fully digital onboarding, multi-currency support, and a unified dashboard, businesses can start accepting payments quickly and manage everything from a single platform.

What is a payment aggregator?

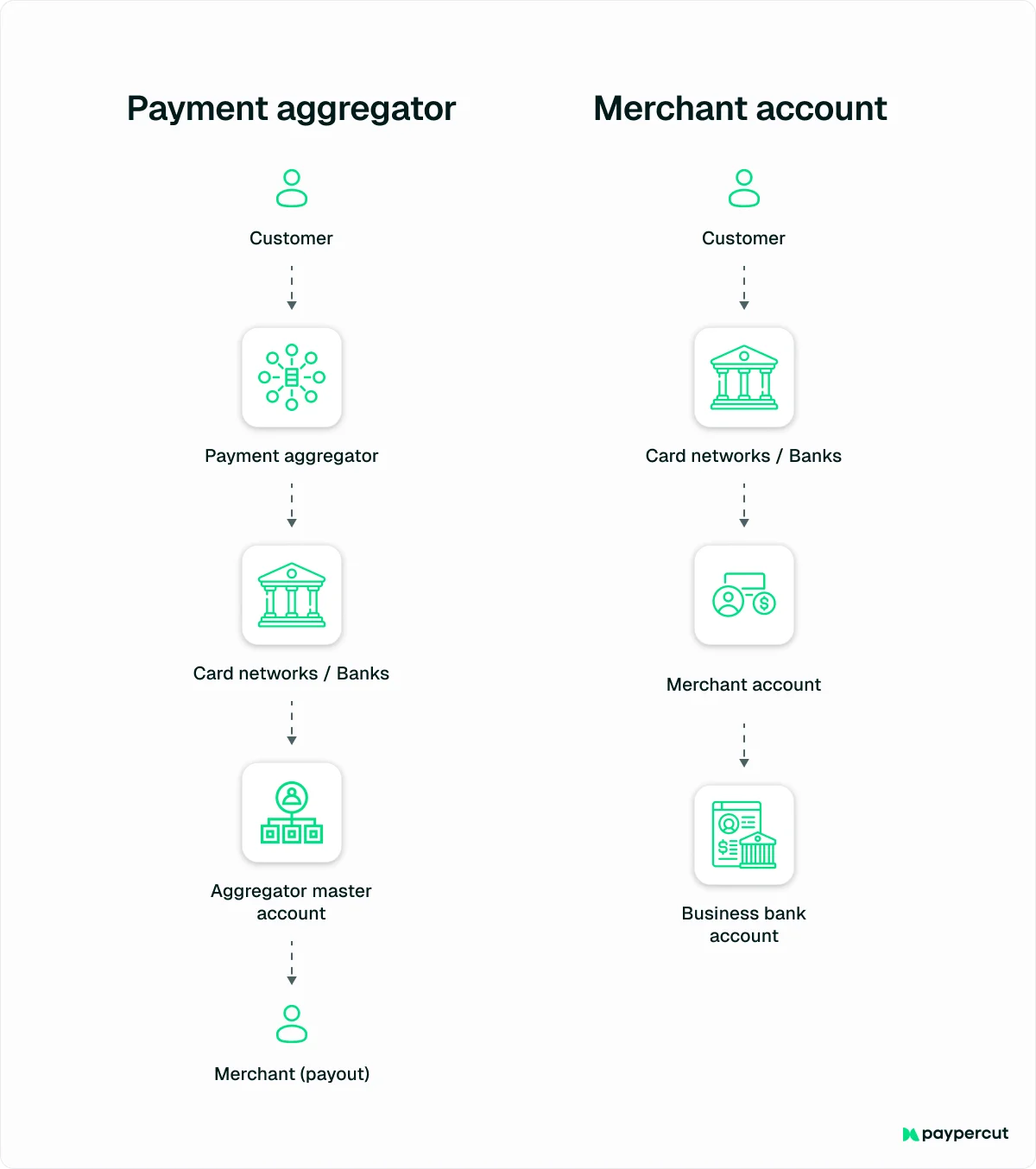

A payment aggregator is a service that lets businesses accept digital payments without opening their own merchant account.

Instead, the business operates as a sub-merchant under the aggregator’s main account, which is sometimes shared by thousands of other merchants.

When it comes to accepting payments, the aggregator acts as a middleman between your business and the payment processor.

So, when a customer pays on your website or checkout page, the transaction goes through the payment aggregator’s system first. The aggregator processes the payment and then sends the funds to your business according to its payout schedule.

What is a merchant account?

A merchant account is a special type of bank account that allows businesses to accept digital payments from customers.

Unlike a payment aggregator, a merchant account is set up specifically for your business.

When your account is approved, you receive a unique merchant ID (MID)—a number used to identify and track your transactions.

The account is created through a payment processor or acquiring bank and connected to your website or checkout system through a payment gateway, which is the technology that securely sends payment data between your store and the banks involved in the transaction.

When a customer makes a payment, the transaction is first authorized by their bank. The funds are then temporarily held in your merchant account before being transferred to your regular business bank account.

Payment aggregator vs. merchant account: 8 key differences

Below, we break down eight key differences in the payment aggregator vs. merchant account comparison to help you understand what sets these two payment models apart and which option may suit your business better.

1. Account setup and approval

With a payment aggregator, account setup is usually fast and simple.

Businesses sign up through an online form, submit basic company details, and complete KYC verification (Know Your Customer), a standard identity check required for financial services.

Because the aggregator operates under a shared master merchant account, businesses don’t need to apply for their own merchant ID. That means there’s no detailed underwriting process for each merchant.

In many cases, businesses can start accepting payments shortly after signing up. With aggregators like Paypercut that offer fully digital onboarding, this means getting verified within days and going live within hours of approval.

Setting up a merchant account is the complete opposite, as this process does require individual underwriting. This includes:

- Reviewing your business model and industry

- Checking expected transaction volumes and average order values

- Assessing chargeback and fraud risk

- Verifying business registration and financial details

As a result, the approval process may take a few days or even weeks for high-risk, specialized, or complex applications.

Once approved, your business receives its own dedicated MID and a payment setup designed specifically for your operations.

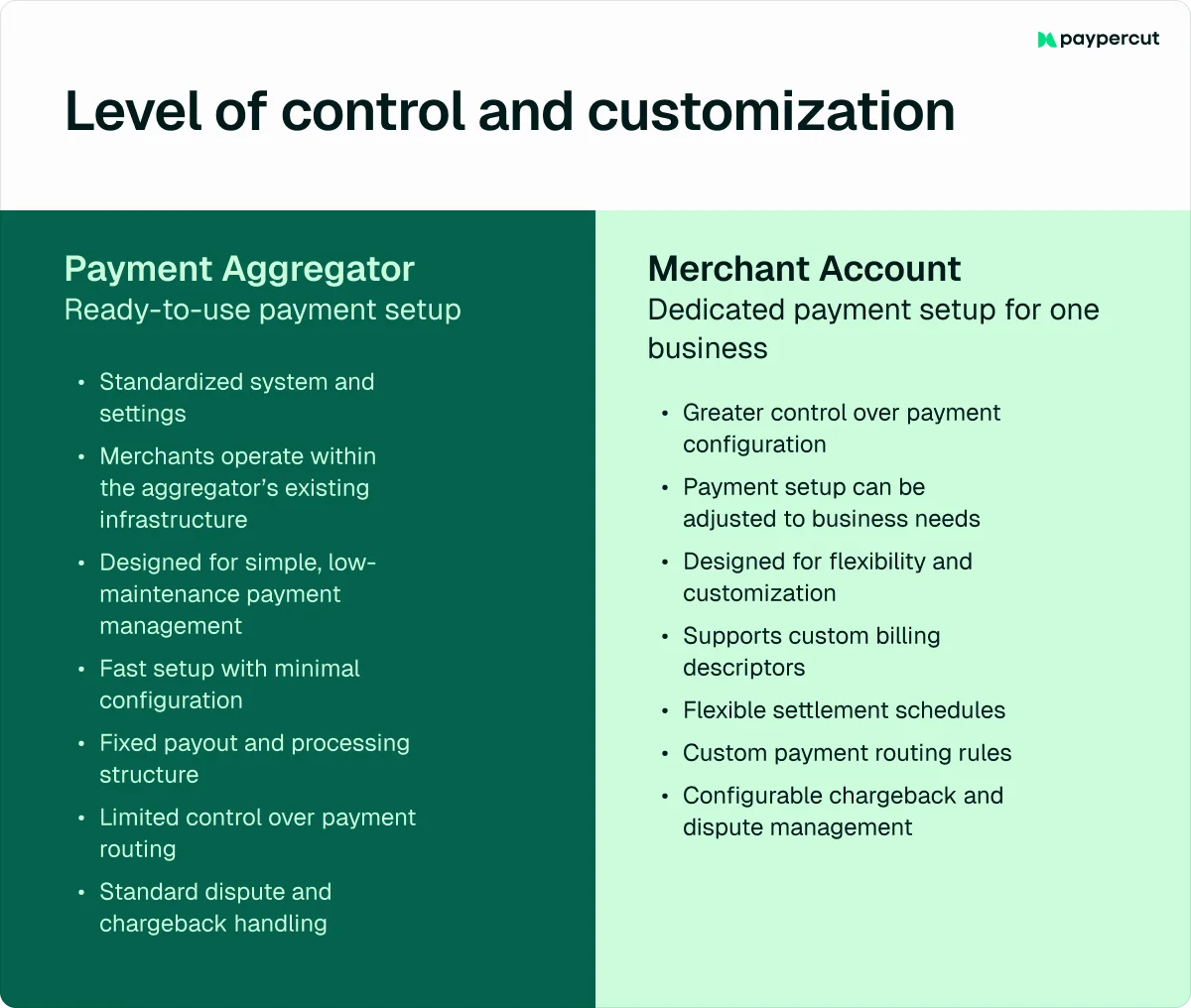

2. Level of control and customization

Payment aggregators provide a ready-to-use payment setup with standardized settings, which means that merchants operate within the aggregator’s existing system.

This structure helps keep payments simple and easy to manage, which is suitable for businesses that want a fast, low-maintenance setup.

As for a merchant account, it typically offers a higher level of control.

Because the account is created specifically for one business, providers can allow more adjustments to the payment setup.

This may include:

- Custom billing descriptors (the name customers see on their bank statement)

- Flexible settlement schedules for payouts

- Custom payment routing rules

- Configurable chargeback and dispute management settings

3. E-commerce and platform integration

Payment aggregators are often designed to work smoothly with popular e-commerce platforms and business tools.

Many providers offer ready-made integrations for platforms like Shopify, WooCommerce, or Magento, as well as plug-ins and APIs that make it easy to connect payments to online stores, marketplaces, or invoicing systems.

This helps businesses add payment functionality without building complex technical integrations.

Merchant accounts can also support e-commerce and platform integrations, but the process often requires working through a separate payment gateway or additional configuration.

This may involve more technical setup and coordination between multiple providers before payments can be fully integrated with an online store.

4. Payout timing and fund settlement

With a payment aggregator, payouts usually follow the provider’s standard payout schedule.

Businesses typically receive funds on a daily, weekly, or scheduled basis, depending on the platform and payout settings.

However, since the aggregator manages payments for many merchants under one system, automated risk checks may occasionally delay a payout while transactions are reviewed.

On the other hand, merchant accounts go through full underwriting before approval, which means fewer risk checks happen after transactions. This typically results in more predictable payout timing.

Many providers transfer funds to the business bank account within one to two business days after a transaction, depending on the acquiring bank and payment method.

Settlement timing can also be configured or negotiated as part of the merchant account agreement.

5. Fees and overall costs

Choosing between a payment aggregator and a merchant account can influence how much a business pays for payment processing, both upfront and over time.

The table below breaks down the main payment processing cost components across payment aggregators and merchant accounts:

⚠️Note: Although payment aggregators are often associated with simple, pay-as-you-go pricing, the actual cost structure can vary between providers.

Some platforms charge activation fees, monthly subscriptions, or additional service fees that may increase the total cost over time.

Paypercut, for example, uses a transparent pricing model with no activation fees, no monthly charges, and no support costs, allowing businesses to pay only for the transactions they process.

6. Scalability and business growth

As businesses grow, their payment volumes, average order values, and geographic reach often increase as well. The payment model you use can influence how easily you handle that growth.

Payment aggregators make it easy to start accepting payments quickly, but rapid growth, such as large spikes in volume or higher-value transactions, may trigger additional reviews or limits as the provider evaluates the activity.

Merchant accounts are often preferred by businesses that require a highly customized payment setup or specific acquiring arrangements.

Because the account is set up specifically for one business, providers can support higher processing volumes and adapt the payment setup as the company expands.

7. Fraud prevention and risk management

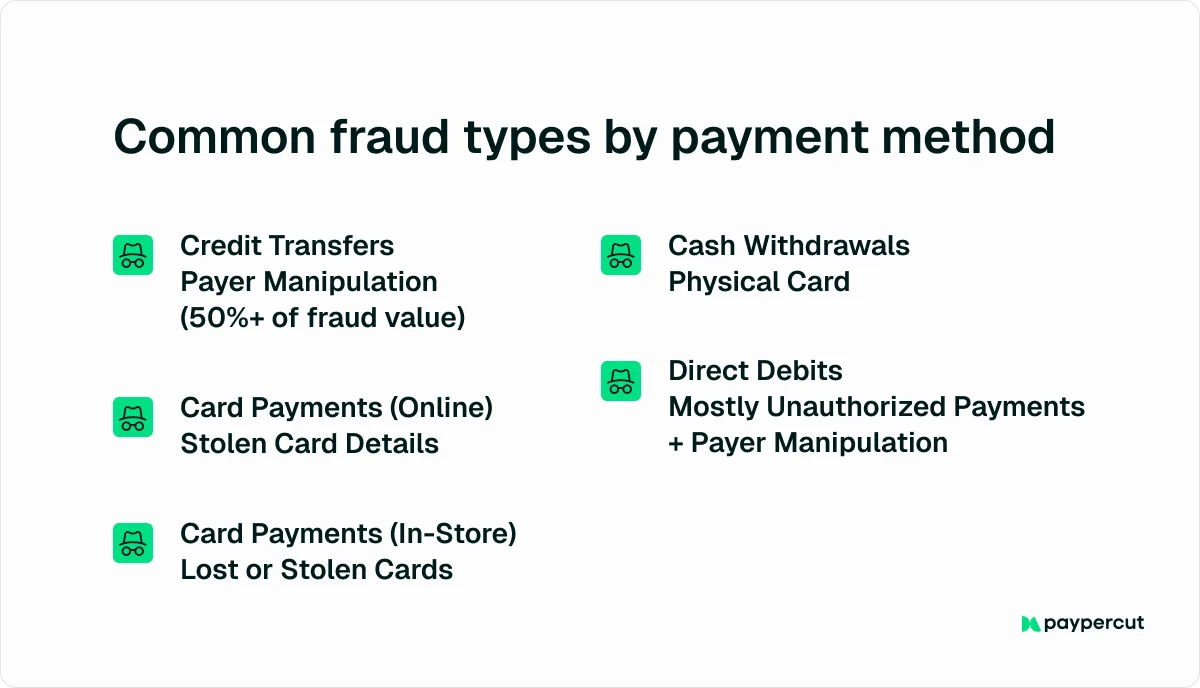

In the European Economic Area, payment fraud reached €4.2 billion in 2024, up from €3.5 billion in 2023, which makes it a growing concern for businesses that accept online payments.

With payment aggregators, fraud prevention is largely handled through automated monitoring systems, with algorithms analyze transactions for unusual patterns.

If suspicious activity is detected, the provider may:

- Delay payouts

- Place a temporary hold on funds

- Restrict the account while the activity is reviewed

These measures help protect the platform from fraud but can sometimes interrupt access to funds during the review process.

A merchant account typically uses a more individualized risk approach.

Since the provider completes detailed underwriting before approving the account, it has a clearer picture of the business’s normal transaction patterns.

If unusual activity appears, the processor may investigate the issue together with the merchant before taking action, which can help resolve fraud concerns while maintaining payment continuity.

8. Support and account assistance

Support models vary significantly between payment aggregators.

Some providers rely primarily on self-service tools and ticketing systems, while others offer dedicated onboarding and direct access to payment specialists.

Choosing a reliable aggregator partner can make a big difference in how quickly issues are resolved and how much guidance businesses receive.

Paypercut, for example, takes a human-first approach to support.

Businesses can speak directly with real support specialists who understand payment processing and the needs of growing companies, rather than relying only on automated chatbots or self-service documentation.

With a merchant account, support is typically individualized.

Since the provider reviews the business in detail during onboarding, support teams often have more context about the merchant’s payment setup and can provide more tailored assistance when issues arise.

Payment aggregator vs. merchant account: Which one is better for your business?

There isn’t a single answer to whether a payment aggregator or a merchant account is better. Each model is designed for different business needs, and the right choice depends on how your company accepts payments and how it plans to grow.

When comparing the two, the decision usually comes down to factors such as:

- Business size

- Transaction volume

- Industry requirements

- Level of control you need

When a payment aggregator may be the better fit

Payment aggregators work well for businesses that want a fast, simple way to start accepting payments without managing complex payment infrastructure.

They provide ready-to-use tools, quick onboarding, and flexible payment features that make them attractive for many modern businesses, including:

- Startups and early-stage businesses

- Small businesses with lower or moderate transaction volumes

- Online-first stores or service providers

- Businesses testing new products or business concepts

- Pop-up shops, temporary projects, or seasonal businesses

- Service-based businesses that take deposits, bookings, or occasional payments

Paypercut, in particular, is designed for online-first businesses that take payments across multiple channels, not just traditional e-commerce checkouts.

This makes it a good fit for businesses such as:

- Online retail stores selling fashion, electronics, beauty, home goods, or niche products

- Restaurants, cafés, bakeries, and catering services accepting bookings, deposits, or event payments

- Beauty and wellness businesses such as salons, spas, fitness studios, and coaching programs

- Mobility and service businesses, including couriers, rental services, and delivery operators

- Nonprofits and charities collecting donations online, at events, or through social channels via payment links

When a merchant account may be the better fit

Merchant accounts are often chosen by businesses that need more customized payment setups and predictable processing conditions, especially as payment operations become more complex.

This may include:

- Established retail stores and restaurant chains

- Multi-location businesses

- High-volume e-commerce brands

- Subscription-heavy SaaS platforms

- B2B companies processing large invoices

- Marketplaces or platforms handling payments for multiple vendors

- Businesses in regulated or higher-risk industries

Get started with Paypercut

While payment aggregators are often associated with startups and smaller businesses, modern payment platforms can also support more complex payment operations. Paypercut works with both growing businesses and established merchants, offering flexible payment setups, local payment methods, multi-currency support, and tailored guidance based on each company's needs.

Whether you're launching a new online store, expanding into new European markets, or looking to simplify an existing payment infrastructure, Paypercut can help you accept payments through a single platform without sacrificing flexibility as you grow.

If you’ve decided that this is the right fit for your business, Paypercut makes it easy to get started.

You can create your account online in just a few minutes and complete a fully digital verification process.

With Paypercut, you also get:

- One platform for multiple payment methods — cards, digital wallets, QR payments, and multiple Buy Now, Pay Later options

- A unified dashboard to manage payments, subscriptions, and reporting in one place

- Flexible checkout options, including hosted checkout, embedded checkout, Express Checkout, and e-commerce plugins

If you’re still comparing options or want guidance on the best setup for your business, you can also schedule a 30-minute consultation with the Paypercut team to discuss your payment needs and growth plans.