Let’s be real, setting up payments can get messy fast.

You need to juggle banks, gateways, security checks, and endless compliance rules just to start accepting money online.

However, understanding the payment aggregator meaning can save you from all that chaos.

In this guide, we’ll break down what a payment aggregator is, how it works, and why more businesses are using it to make online payments smoother and more reliable.

Key Takeaways

- Payment aggregators make digital payments simple and fast

They let merchants accept cards, wallets, and BNPL through one platform, taking care of all the technical, security, and compliance requirements so businesses can start accepting payments quickly without multiple bank setups.

- SMEs, ecommerce stores, and subscription platforms benefit the most

Small and medium businesses, online retailers, and recurring payment models gain from faster onboarding, lower costs, and automated billing that improves customer experience and retention.

- They boost security while cutting operational costs

Aggregators handle fraud checks, PCI DSS compliance, and data protection, helping businesses lower chargebacks and save up to 15% annually through simplified payment management.

- The right aggregator should be reliable, scalable, and compliant

Look for providers with proven uptime, easy API integration, regulatory certifications, and local payment support to ensure smooth transactions and long-term growth.

- Paypercut helps Central & Eastern European SMBs simplify payments

With fast onboarding, BNPL integration, recurring billing, and local currency support, Paypercut is the all-in-one solution for growing businesses that want secure, localized, and effortless payment management.

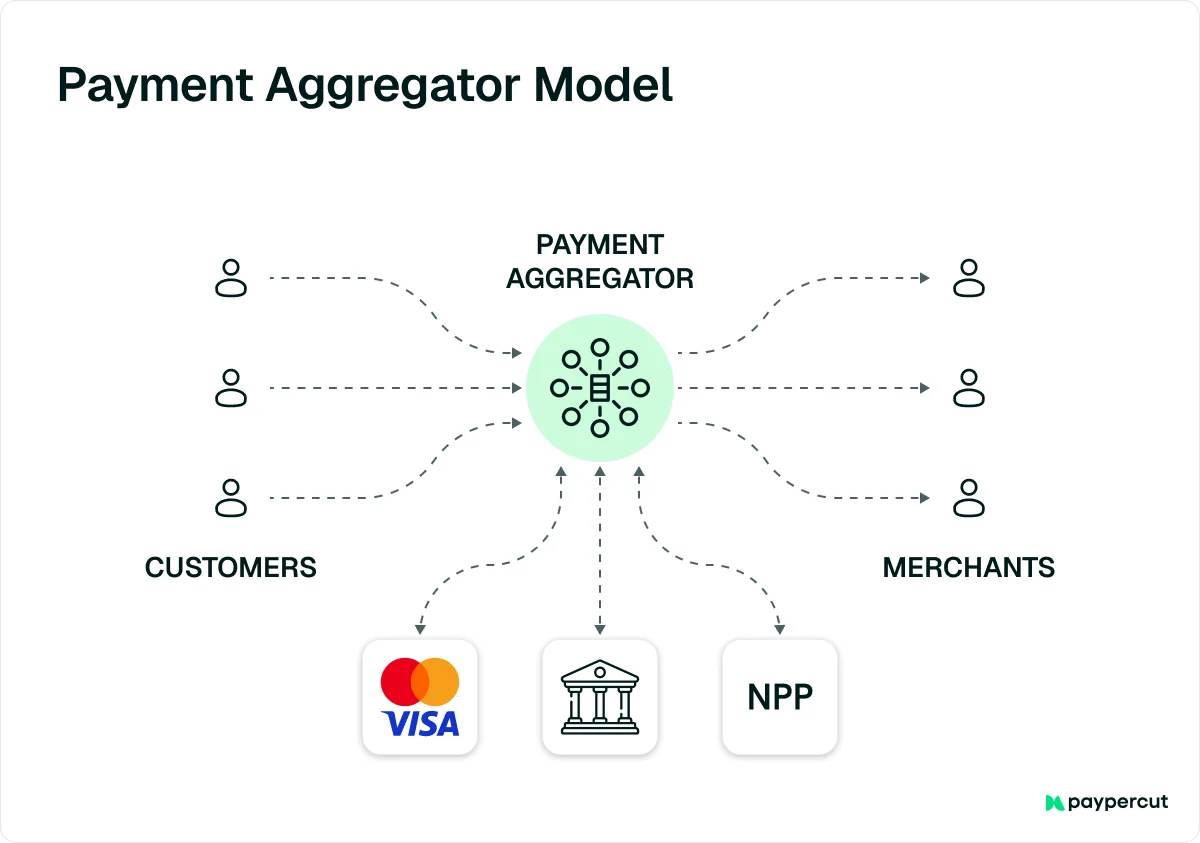

What is a payment aggregator?

A payment aggregator is a service provider that enables merchants to accept multiple online payment methods, such as credit cards, debit cards, and digital wallets, through a single platform.

It streamlines the payment process by handling technical and regulatory requirements, enabling businesses to quickly accept digital payments without the hassle of setting up separate accounts with different banks or processors.

What types of businesses use payment aggregators?

Payment aggregators are used by a wide variety of businesses across different industries thanks to their flexibility and simplicity. However, some types of businesses tend to benefit more from using them:

1. Ecommerce businesses

Online retailers and ecommerce platforms rely heavily on payment aggregators to process secure, seamless transactions.

Aggregators make it easy to accept credit cards, digital wallets, and other online payment options through a single integration, helping businesses streamline checkout and improve customer experience.

Studies show that Ecommerce businesses using payment aggregators report a 23% reduction in cart abandonment rates, thanks to faster checkout and greater trust at payment screens.

2. Small and medium-sized enterprises (SMEs)

For small businesses, startups, and local service providers, payment aggregators offer a quick, affordable way to start accepting digital payments.

They eliminate the need for traditional merchant accounts, which can be costly and time-consuming to set up, making them ideal for SMEs that want simplicity and speed.

Around 65% of small businesses now use payment aggregators, compared to 35% that rely on traditional payment gateways

3. Mobile app developers

Developers of mobile apps, such as those for gaming, travel, food delivery, or ticket booking, often use payment aggregators to enable secure in-app purchases and transactions. This ensures users can pay easily within the app without being redirected elsewhere.

4. Subscription-based services

Businesses built on recurring payments, like streaming platforms, SaaS companies, membership sites, coworking spaces, and fitness studios, use payment aggregators to automate subscription billing and manage renewals.

Many aggregators also offer built-in tools for recurring payments, reducing manual work and billing errors.

In fact, subscription-based businesses integrated with payment aggregators see 25% higher customer retention rates, due to automated renewals and fewer failed payments.

5. Marketplaces and sharing economy platforms

Platforms that connect buyers and sellers, such as ride-sharing services, accommodation booking sites, and freelance job portals, depend on payment aggregators to handle complex payment flows.

Aggregators make it possible to collect payments from customers and distribute funds to multiple vendors or service providers efficiently.

6. Nonprofit organizations

Nonprofits and charities often use payment aggregators to accept online donations securely. These platforms simplify the donation process and offer reporting features that help organizations track contributions and donor activity.

Benefits of using a payment aggregator

A payment aggregator offers numerous advantages that simplify and enhance how businesses accept and manage payments.

- Easy setup – Businesses can quickly sign up and start accepting payments, often within 2–3 days, compared to the 2–3 weeks typically required for traditional merchant accounts.

- Seamless payment experience – Aggregators bring multiple payment methods together on a single platform, allowing customers to pay using their preferred option. This flexibility enhances convenience and can boost conversion rates.

- Cost-effective solution – Payment aggregators typically have lower upfront costs and remove the need to invest in specialized payment hardware or software.

They also help businesses avoid direct agreements with multiple payment processors, saving up to 15% in operational costs annually through reduced fees and simplified management.

- Faster go-live – Businesses can integrate payment capabilities into their websites or apps within days, significantly cutting time to market and allowing for quicker launches or updates.

- Secure and compliant – Aggregators manage sensitive payment data and follow strict security standards, reducing compliance burdens for businesses.

Their advanced fraud detection systems help cut chargebacks by up to 30%, offering both protection and peace of mind.

- Added functionality – Many aggregators provide advanced tools such as recurring billing, subscription management, fraud detection, and detailed reporting, helping businesses streamline operations and make data-driven decisions.

- Scalable for growth – As your business grows, payment aggregators can easily accommodate higher transaction volumes and evolving business models, making them suitable for startups and enterprises alike.

How payment aggregators work

Now that you understand what a payment aggregator is and how it benefits your business, let’s take a closer look at how it actually works behind the scenes:

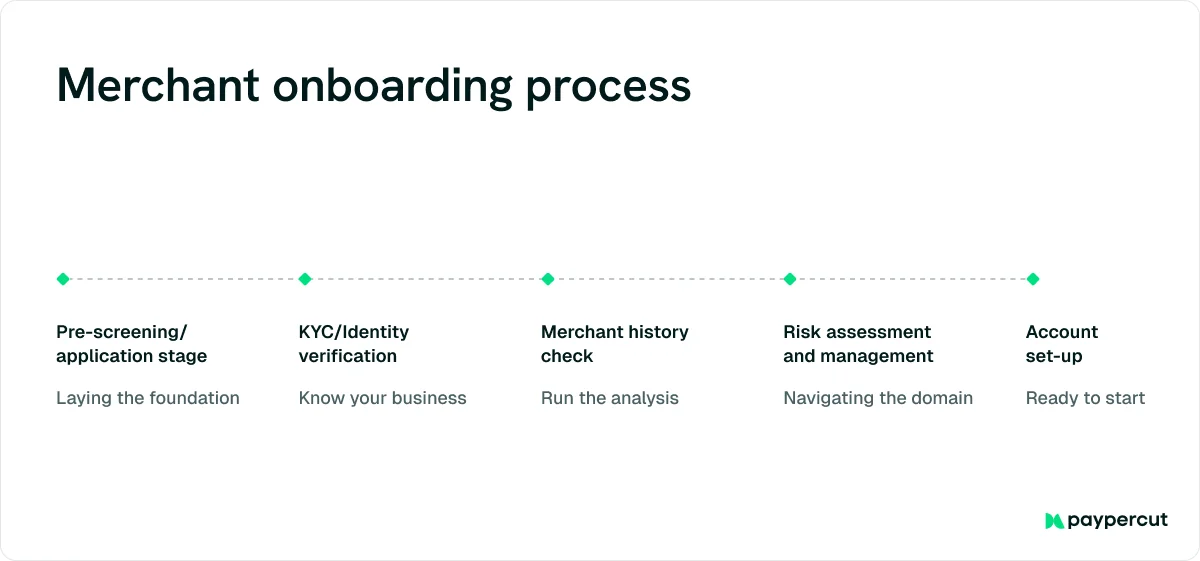

Step 1: Merchant onboarding

To start accepting online payments, you first need to sign up with a payment aggregator.

Once onboarded, your transactions will flow through the aggregator’s nodal account, which is maintained with a partner bank.

This nodal account acts as a central pool where customer payments are received before being transferred to individual merchants.

While the bank manages the nodal account, it doesn’t have visibility into the details of each transaction, it only sees the overall inflows and outflows.

Step 2: Customer proceeds to checkout

When a customer checks out on your website, they’re directed to the payment window.

Here, they select their preferred payment method (credit card, UPI, wallet, etc.) and enter their details.

The payment aggregator then tokenizes this sensitive information to keep it secure and runs initial fraud checks to detect suspicious activity.

Step 3: Transaction processing behind the scenes

Once the customer submits payment, the aggregator sends the transaction details to its partner bank.

That bank forwards the payment request to the relevant card network (like Visa or Mastercard) through a payment processor.

Step 4: Fraud verification by the card network

Next, the card network performs additional fraud checks based on the customer’s previous transactions and risk patterns.

Some networks also use large fraud-detection databases to identify unusual behavior. If everything looks good, the transaction information moves on to the customer’s issuing bank.

Step 5: Customer’s bank reviews and responds

The customer’s bank receives the transaction details and verifies whether:

- The customer has enough balance, and

- The payment details are valid.

The bank then sends back a response, approved or declined, following the same route:

Customer’s bank → Card network → Aggregator’s bank → Payment aggregator → Merchant.

Once the merchant receives the status, it’s displayed to the customer instantly.

Step 6: Funds are requested

If the transaction is approved, the aggregator’s partner bank requests the funds from the customer’s bank.

These funds are then temporarily held in the nodal account until settlement.

Step 7: Settlement to the merchant

Finally, at the end of the business day, the payment aggregator transfers the collected funds to the merchant’s account as a lump-sum payment for all successful transactions.

Some aggregators also offer instant or same-day settlements for faster access to funds.

How to choose the best payment aggregator for your business

While most aggregators offer similar core services, what truly matters is how well they perform, comply with regulations, and adapt to your growth needs worldwide.

Here’s what to look for:

✅ Reliability & performance

Choose an aggregator with a proven record of uptime, transaction speed, and security to ensure seamless payment experiences across all markets.

You can check this on:

- The aggregator’s status or uptime page

- Customer reviews on trusted sites like G2 or Capterra

- Industry reports or benchmark studies from Forrester, Gartner, or IDC

✅ Ease of integration

Select a provider with clear documentation, strong APIs, and ready-to-use plugins that simplify setup and reduce time to market.

You can check this on:

- The aggregator’s developer documentation

- Their sandbox or demo environment for testing integration

- Developer community feedback on GitHub, Stack Overflow, or fintech forums

✅ Regulatory compliance

Partner with an aggregator that adheres to international financial and data protection standards such as PCI DSS, GDPR, and AML/KYC.

You can check this on:

- The PCI Security Standards Council website for official certifications

- SOC 2 or audit summaries available upon request from the provider

- Local financial regulatory registries or government licensing databases

✅ Scalability

Ensure the aggregator can handle increasing volumes, new currencies, and multiple payment methods as your business expands globally.

You can check this on:

- The aggregator’s case studies or customer success stories

- Their API rate limits and performance documentation

- References from existing enterprise clients with similar growth patterns

✅ Customer support & SLAs

Choose a provider offering 24/7 multilingual support and transparent service level agreements (SLAs) for uptime, response time, and resolution.

You can check this on:

- A sample SLA provided by the aggregator

- Their support response channels (chat, email, or phone)

- User feedback and ratings on Trustpilot, G2, or Capterra

✅ Market-specific features

Work with an aggregator that supports local payment preferences, currencies, and alternative methods to meet customer needs in every region.

You can check this on:

- The aggregator’s supported payment methods list

- Market data and payment reports like Worldpay’s Global Payments Report or Statista

- The provider’s coverage map or localization documentation

Make payments easy for you and your customers with Paypercut

Now that you know the meaning of a payment aggregator and how it works, the next step is choosing the one that can truly support your business as it grows.

Whether you run an online shop, mobile app, or subscription-based service, you need to find the one that makes payments simple, secure, and effortless for both you and your customers.

If you are a small or medium-sized business in Central or Eastern Europe looking for a simple, localized, and flexible way to accept payments, Paypercut is the perfect choice for you.

Paypercut empowers merchants to accept cards, wallets, and Buy Now, Pay Later (BNPL) options through a single platform, eliminating the need for separate integrations or contracts.

What makes Paypercut unique is its BNPL aggregator, the first of its kind in the region, which connects merchants to multiple BNPL providers via one setup, improving approval rates and cross-border flexibility.

Here’s what Paypercut brings to your business:

- All-in-one payment platform – Manage BNPL, card, and digital wallet payments from a single dashboard. Get local settlements in your currency (BGN, RON, HUF, PLN, CZK, EUR, and more).

- Fast onboarding, zero hassle – Get started in minutes with simple integration options via API or ready-made plugins for WooCommerce, OpenCart, and Shopify.

- Localized experience – Offer payments in local currencies and languages, with checkout flows tailored to your market’s habits and regulations.

- Recurring and subscription payments – Automate billing for memberships or repeat services to save time and keep revenue flowing.

- Clear merchant dashboard – Track payments, payouts, and performance in real time for full transparency.

- Built for SMBs – Enjoy friendly onboarding support, clear documentation, and real people to guide you at every step.

Start accepting payments the smart way.

Join Paypercut today and give your customers a faster, safer, and simpler checkout experience!

FAQs:

1. What is the difference between a Payment Bank and a Payment Aggregator?

A Payment Bank is a regulated financial institution that accepts deposits and enables digital transactions, but cannot issue loans or credit cards.

A Payment Aggregator, on the other hand, provides a platform that allows merchants to accept payments from multiple methods, such as cards, UPI, and wallets, without separate integrations with each bank.

2. What is the difference between a Payment Gateway and a Payment Aggregator?

A Payment Gateway is a secure technology that transmits a customer’s payment details from a website or app to the bank or processor.

A Payment Aggregator builds on this by integrating multiple payment options into a single system, making it easier for merchants to manage all transactions through a unified interface.

3. What is the usual payment aggregator fee?

Payment aggregators typically charge merchants based on their total transaction volume (gross processing volume). Because payments are processed under the aggregator’s main account, merchants may have lower transaction limits than with dedicated merchant accounts.