Buy Now, Pay Later (BNPL): How It Works & Examples [Guide]

Looking for a smarter way to boost conversions and reduce cart abandonment?

Retailers offering Buy Now, Pay Later (BNPL) options have seen average order values increase by 6.42%, according to recent research, as flexible payment plans make it easier for shoppers to complete their purchases.

Yet, many businesses still wonder how BNPL actually works, what it costs, and whether it’s the right fit for their customers.

In this guide, we’ll break down what BNPL is, how it operates, and why it’s rapidly reshaping the future of retail.

Key Takeaways

- BNPL drives higher sales and customer conversion

Offering Buy Now, Pay Later (BNPL) can lift conversion rates by 30% and boost average order values. By breaking large purchases into smaller installments, customers feel more comfortable completing their checkout.

- It expands your reach to younger, digital-first shoppers

BNPL strongly appeals to Gen Z and Millennial buyers, over half of whom already use it. These demographics favor flexible, credit-free payment methods and often choose merchants that offer BNPL options.

- Merchants benefit from upfront payment and reduced risk

Businesses receive full payment right away from the BNPL provider, improving cash flow and reducing exposure to fraud or default. The provider assumes financing and collection responsibilities, simplifying operations.

- BNPL helps bring customers back and build loyalty

Flexible payment options make shopping feel easier and more affordable, encouraging customers to return. This can boost repeat purchases and customer lifetime value, especially in categories like fashion, electronics, and home goods.

- Simplify BNPL adoption with Paypercut’s all-in-one solution

Paypercut lets you offer cards, digital wallets, and BNPL through a single integration. As a first-of-its-kind BNPL aggregator in Central and Eastern Europe, it connects you to multiple providers, offers localized settlements, and provides real human support, helping you scale faster without added complexity.

What is Buy Now, Pay Later (BNPL)?

Buy Now, Pay Later (BNPL) is a flexible payment solution that lets customers purchase products or services without paying the full amount upfront. Instead, the total cost is divided into smaller, fixed installments over time, often with no interest or fees when payments are made on schedule.

For instance, a shopper purchasing a €100 item might pay €25 at checkout, followed by three additional payments of €25 every two weeks or a month.

.png)

For merchants, BNPL offers a seamless experience. You receive the full payment amount upfront (minus any applicable fees).

At the same time, the BNPL provider handles the financing, installment management, and payment collection, allowing you to focus on running and growing your business.

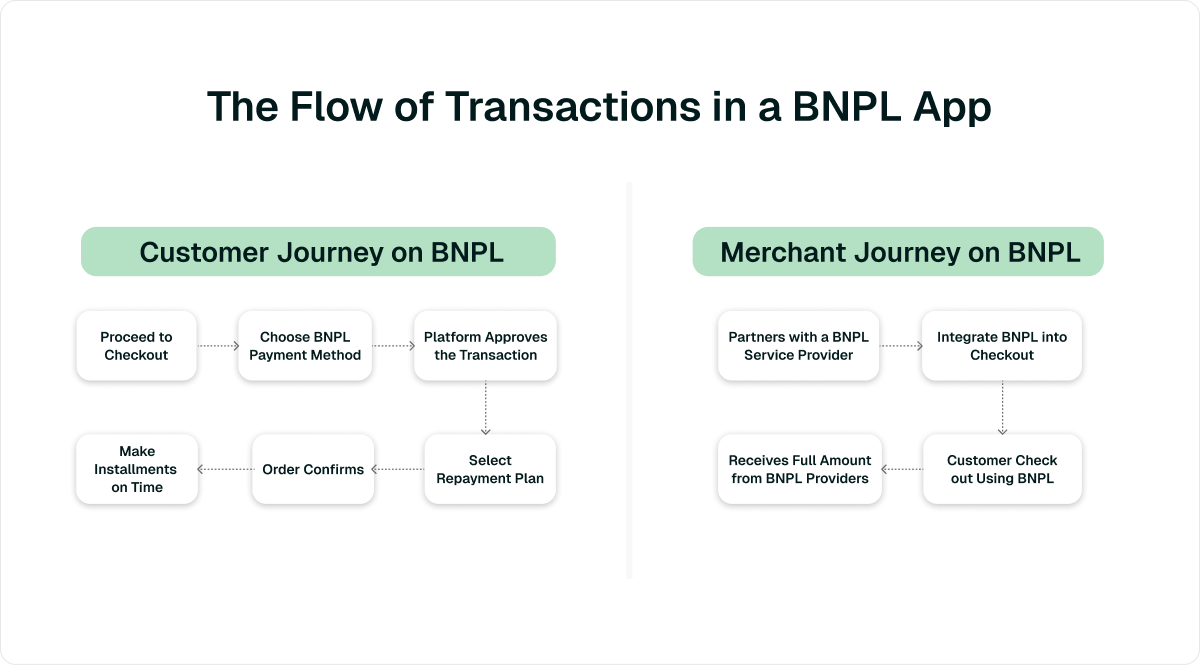

How does BNPL work?

Now that you know what Buy Now, Pay Later is, let's explore how this process actually works:

Step 1: Customer selects BNPL method at checkout

When shoppers are ready to complete their purchase, they’ll see Buy Now, Pay Later listed as one of the available payment options, alongside familiar methods like credit cards or PayPal.

By selecting this option, customers can choose from various installment offers. For example:

- Offer 1: 3 payments

- Offer 2: 5 payments

- Offer 3: 10 payments

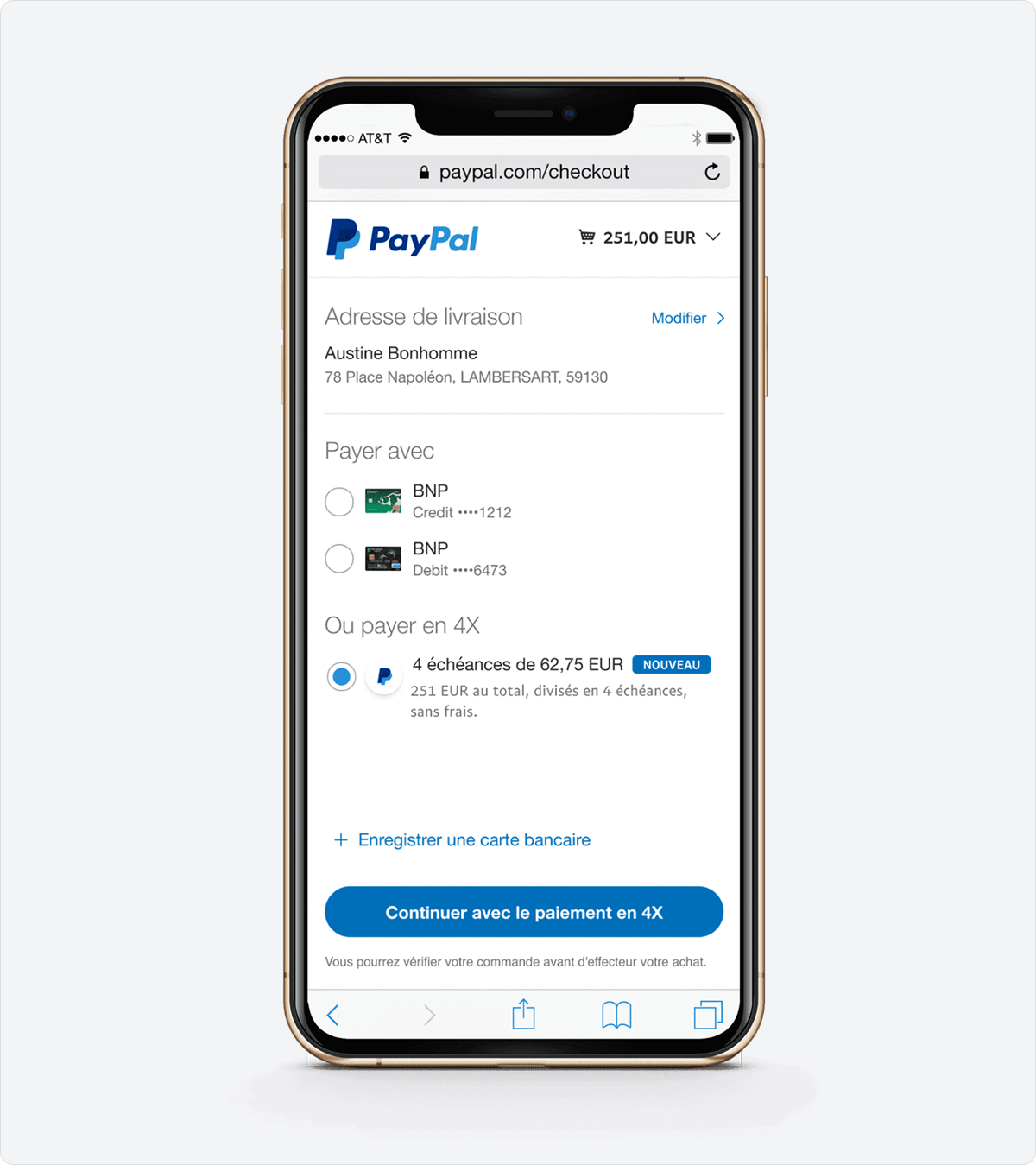

Step 2: Quick approval

After choosing a BNPL option, the customer is usually asked to sign up or log in to the provider’s platform. The provider then runs a quick check to confirm the customer’s eligibility for the purchase amount.

One of BNPL’s main advantages is its low barrier to entry, since it doesn’t require a lengthy application or hard credit check. In most cases, approval is nearly instant, allowing customers to complete their purchase within seconds.

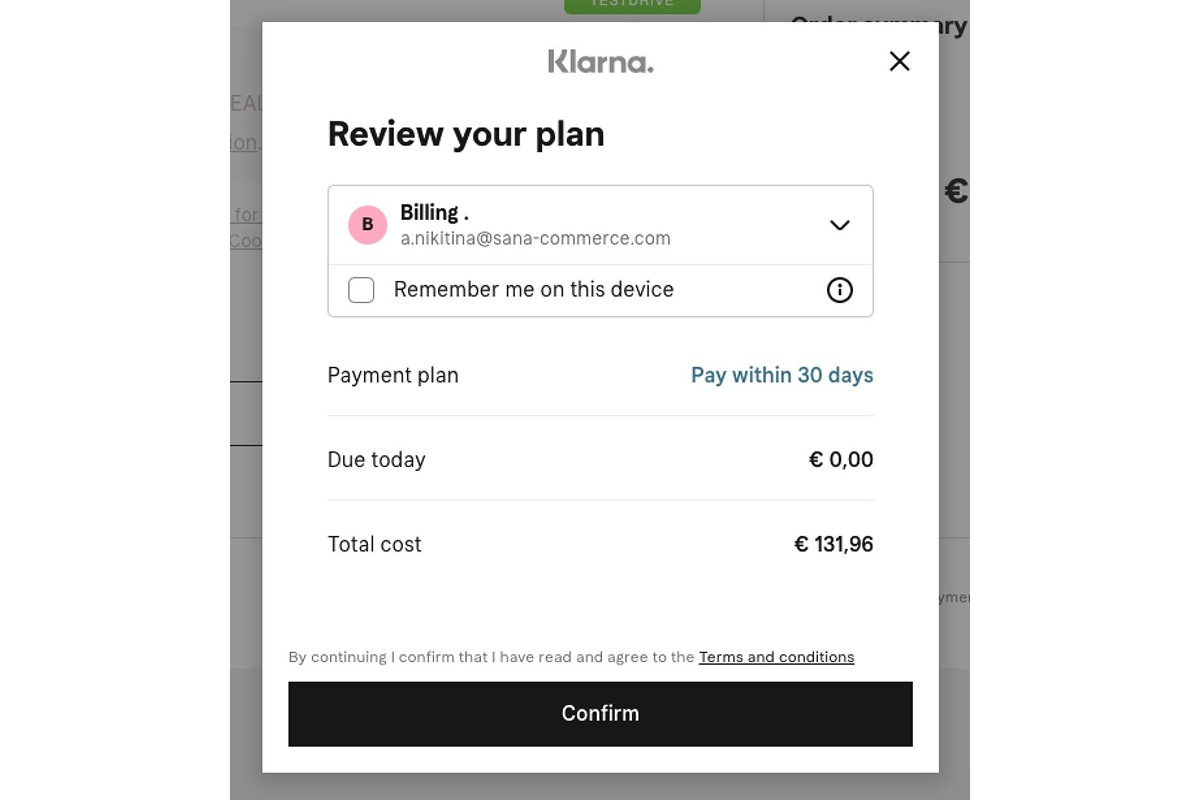

Step 3: The Initial payment is made

Once the customer is approved, they typically make an initial payment, often about 25% of the total purchase.

For example, if an item costs €200, the customer might pay €50 upfront as the first of four installments. This initial payment is typically charged to the debit card, credit card, or bank account associated with their BNPL account.

Step 4: Merchant gets paid upfront

BNPL provider pays the merchant the full purchase amount (minus a small processing fee) shortly after the transaction. This means your business doesn’t have to wait for the customer to complete all their installment payments.

Step 5: Customer pays the remaining installments to the BNPL provider

After making their initial payment, the customer pays the remaining installments to the BNPL provider on the agreed schedule.

These are often automated, with reminders or tracking available through the provider’s app. As long as payments are on time, there are typically no interest charges or extra fees.

Step 6: Completion and post-sale adjustments

Once all installments are paid on schedule, the loan is complete. If the customer returns a product or receives a refund, the process may vary, but typically:

- The merchant works with the BNPL provider to adjust the payment plan.

- Remaining installments may be canceled.

- Refunds may be issued for amounts that have already been paid.

From the customer’s perspective, everything is managed through the BNPL provider’s app or platform, where they can view updates and track any changes to their payments.

Popular BNPL models and examples

Buy Now, Pay Later (BNPL) isn’t a one-size-fits-all solution. It comes in several formats designed to fit different shopper needs and purchase types.

Let’s explore the most common BNPL models, how they work, and real-world examples of the brands and platforms that have made each one popular.

1. Pay-in-4 / Short-term installment plans

This is the most familiar Buy Now, Pay Later model. The total purchase amount is divided into four equal payments, one due at checkout, and the remaining three every two weeks over a six- to eight-week period.

These plans are typically interest-free as long as payments are made on time, making them especially attractive for small to mid-sized purchases such as clothing, beauty products, or electronics.

📌 Example

PayPo (Poland) allows shoppers to split their purchases into multiple installments, depending on the order value, typically ranging from 3 to 12 payments. For example, a €600 order can be paid in installments of €150 per month over four months, with no interest if the payments are made on time.

2. Pay-later (Deferred payment)

With this model, shoppers receive their items immediately but have the option to pay the full amount later, typically within 14 to 30 days.

It functions as a short-term credit line that allows customers to “try before they buy,” making it especially useful for purchases of fashion or home goods.

Payments are interest-free if made on time, though late fees may apply after the due date.

📌 Example

Klarna’s “Pay in 30 Days” plan lets customers order items, try them out, and only pay if they decide to keep them.

3. Long-term financing plans

This model extends repayment periods over 3 to 24 months (or longer), making it ideal for higher-ticket items such as electronics, furniture, or travel.

These plans may include interest or fixed fees, depending on the customer’s credit profile and the merchant’s agreement with the BNPL provider.

📌 Example

Twisto (Czech Republic, Poland) offers flexible installment plans for larger purchases. Through its Twisto Splátky feature, customers can split payments over 3 to 12 months for purchases above 1,000 CZK.

4. Subscription / Revolving credit BNPL

This version of BNPL functions like a digital credit line, enabling users to make multiple purchases up to a specified limit and repay the balance over time. It’s best suited for frequent shoppers who value flexibility and convenience.

Customers often make minimum weekly or monthly payments and may be charged interest or account fees if balances aren’t cleared.

📌 Example

Mokka (Poland, Romania, Bulgaria) follows this model. Users receive a spending limit (e.g., €1,000) that can be reused across multiple purchases. As they repay, their balance refreshes, providing ongoing access to funds and flexible shopping across partner merchants.

4 Key benefits of BNPL services

Buy Now, Pay Later has quickly become a preferred payment option for customers and a valuable tool for merchants. Let’s explore the key benefits of BNPL:

1. Increased sales and conversion

For businesses, BNPL can significantly increase conversion rates and average order values by reducing the “sticker shock” of a large upfront payment. In fact, merchants offering BNPL often see 30% higher conversion rates on average.

2. Attracting new customers

Offering BNPL helps merchants reach shoppers who might not otherwise purchase, including younger consumers who prefer alternatives to credit cards.

In fact, 64% of Gen Z and 75% of Millennials have used BNPL, indicating that flexible payment options strongly appeal to these younger demographics.

3. Immediate full payment and better cash flow

With BNPL, merchants receive full payment upfront from the provider rather than waiting for installments to be completed. This improves cash flow and eliminates the risk of customer nonpayment, as the BNPL company assumes this risk.

4. Fraud protection and reduced risk for merchants

BNPL providers handle most of the fraud and non-payment risk themselves, so merchants don’t get hit with unexpected losses. They also use built-in fraud checks and underwriting to keep chargebacks low, making payments more predictable.

Challenges and Risks of BNPL

No financial solution is perfect, and BNPL has its share of challenges and potential downsides. Both merchants and customers should understand these key risks before using Buy Now, Pay Later:

- Integration and accreditation challenges – Implementing BNPL requires time, technical resources, and compliance steps to ensure smooth and secure integration.

- Confusing terms from multiple providers – With many BNPL providers offering different fees and conditions, merchants can struggle to compare options and choose the right partner.

- Encouragement of consumer debt – BNPL can increase sales but may also lead to customer over-borrowing and defaults, creating reputational risks and compliance pressures under new EU regulations.

How do you choose a BNPL solution for your needs?

Selecting the right Buy Now, Pay Later provider depends on the types of items you sell, their prices, and your customer base. When evaluating providers, consider the following:

1. Repayment flexibility

BNPL services vary in how they structure payments. Some allow customers to pay over a few weeks, while others spread payments out for several months or even years.

- If your products are higher priced, look for a provider that supports longer repayment periods, such as monthly installments over six months.

- If your average sale is lower, a shorter plan, like four payments over six weeks, can keep things simple and manageable for customers.

2. Spending limits

Each provider sets its own credit thresholds, and customers also have individual limits based on their history and credit profile.

Select a provider whose limits align with your typical order size, ensuring your customers have sufficient available credit to complete their purchases.

3. Regional coverage

Consider where your customers are based. Some BNPL providers focus on specific regions, while others operate globally.

You might need more than one provider to reach all your markets. It can also be helpful to opt for the most popular option in each area. For instance, Twisto dominates in the Czech Republic, while Klarna is a favorite across Germany and the Nordic countries.

How to set up BNPL for your checkout?

Now that you know what BNPL is, you can easily understand why it’s become such a key part of modern shopping.

But for many small and mid-sized merchants, adopting it still feels complicated. Between juggling multiple providers, managing technical integrations, and navigating fees, what should be a growth driver can quickly turn into an operational burden.

That’s exactly why we built Paypercut!

With a single, seamless integration, Paypercut enables merchants to accept cards, digital wallets, and Buy Now, Pay Later options through one secure platform.

As the first BNPL aggregator in Central and Eastern Europe, Paypercut connects you to multiple trusted BNPL providers at once, helping you reach more customers, boost approval rates, and scale effortlessly across borders.

Paypercut’s transparent pay-per-transaction pricing, flexible terms, and real human support mean you can offer modern payment options without added complexity or long-term commitments.

How Paypercut helps your business grow

🟢 One integration, multiple BNPL options – Connect to several BNPL providers instantly through a single API or plugin, improving acceptance rates and flexibility for customers.

🟢 Localized payments and settlements – Operate seamlessly across Bulgaria, Greece, Romania, Czechia, and beyond, with local currency settlements to reduce FX risk.

🟢 Zero lock-in, pay-as-you-go model – No setup fees or contracts, you only pay a small percentage per transaction.

🟢 Flexible payment options – Accept card payments, Apple Pay, Google Pay, recurring billing, and BNPL, all in one platform.

🟢 Merchant-funded BNPL options – Offer installments even in markets without local providers, while maintaining full control over risk and approval.

🟢 Partner revenue opportunities – Earn revenue by onboarding other merchants through Paypercut’s partnership program.

🟢 Human support and simple setup – Get personal onboarding assistance, intuitive dashboards, and plugins for WooCommerce, OpenCart, and Shopify.

Contact us today and upgrade your checkout with flexible BNPL options!

FAQs:

Do Buy Now, Pay Later payment methods affect customers credit score?

Most Buy Now, Pay Later (BNPL) services do not significantly impact customers’ credit score as long as payments are made on time. However, missed payments or hard credit checks by certain providers can negatively affect their credit history and lower your score.

How do Buy Now, Pay Later services make money?

BNPL providers earn revenue from both merchants and customers. Businesses typically pay setup and transaction fees, while customers may incur interest charges or late fees if payments are not made on time.

What happens if a customer misses a Buy Now, Pay Later payment?

Missing a BNPL payment can result in their account being frozen and may lead to additional fees or debt collection efforts. Continued missed payments could also be reported to credit bureaus, potentially harming their credit score.