Have you ever wondered which is a better fit for your business, a payment gateway or a payment aggregator?

If you’ve been setting up online payments, it’s easy to get lost in the jargon and not know which option to choose.

The truth is, there are several important differences between the two, from how they process payments to how quickly you receive your funds.

In this article, we’ll break down payment aggregator vs payment gateway to help you understand which option best fits your needs.

Payment Aggregator vs Payment Gateway: Overview

Before we dive deeper into key differences between payment aggregators and payment gateways, here is a quick overview of what awaits you:

What is a payment aggregator?

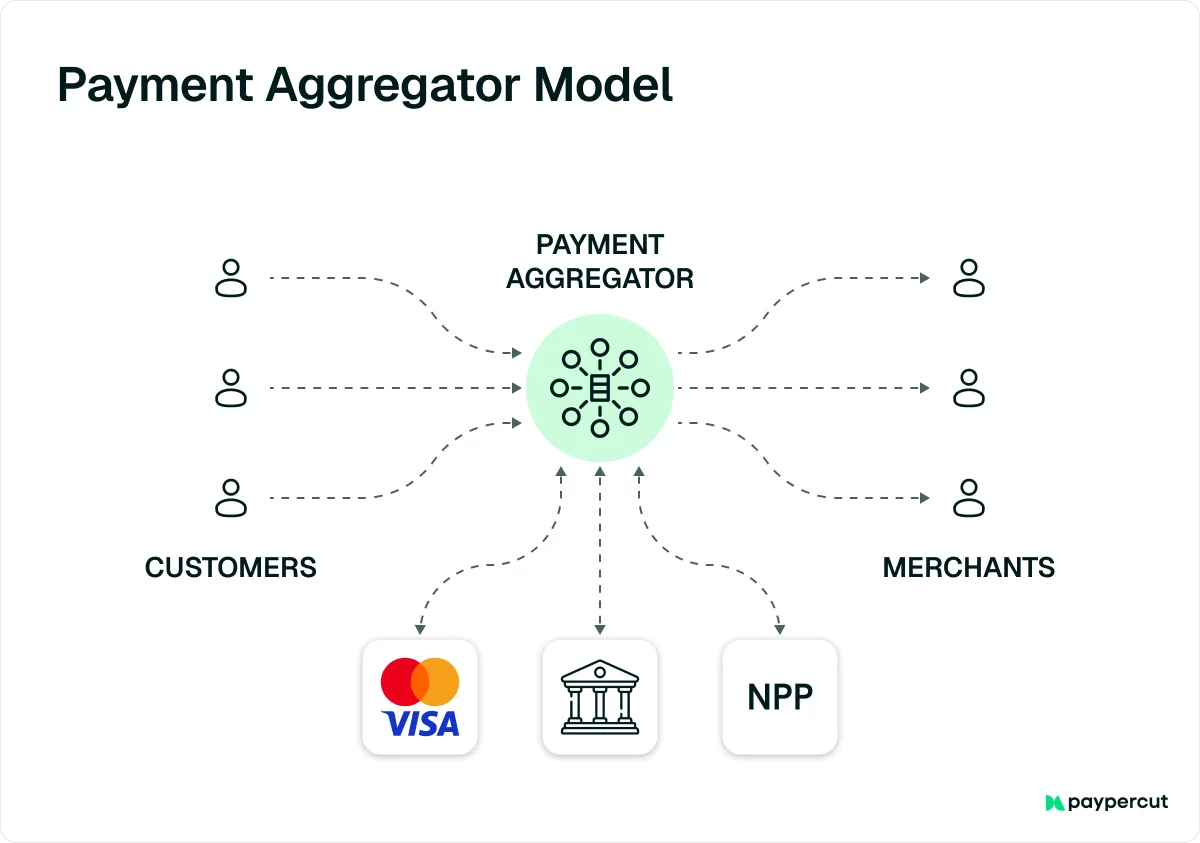

A payment aggregator is a fintech company that helps businesses easily accept electronic payments.

In the past, setting up the ability to take credit card payments required a lengthy process with banks, involving credit checks and compliance reviews. Payment aggregators simplify this by managing those technical and regulatory steps for the business.

As a result, companies, especially small and medium-sized ones, can start accepting payments quickly and with far less hassle.

How does a payment aggregator work?

Payment aggregator handles everything from onboarding to payment processing and fund transfers, creating a simple, all-in-one solution.

Here’s how the process works:

1. Account setup and verification

A business starts by signing up with a payment aggregator and submitting basic details along with any required documents. The aggregator then verifies the business’s identity, checks for compliance, and assesses risk to protect against fraud.

2. Platform integration

Once approved, the aggregator provides easy integration tools like APIs or plugins to connect the business’s website or app. This makes it simple for customers to pay using various methods such as credit cards, debit cards, or digital wallets.

3. Transaction processing

When a customer makes a payment, the aggregator securely captures the payment details and sends them to the right payment processor or bank. The processor then approves and completes the transaction, moving the money from the customer’s account to the merchant’s account.

4. Funds settlement

After transactions are processed, the aggregator ensures the funds are transferred from the bank to the business’s account. While the exact timing can vary, most businesses receive their payments within a few business days.

5. Data and reporting

Many payment aggregators offer helpful dashboards and reports that show sales and transaction data. These insights make it easier for businesses to track performance and make smarter decisions.

6. Additional features and services

Some aggregators go beyond basic payment processing and offer features like recurring billing, subscription management, fraud protection, and customer support. These extra tools help businesses save time and deliver a better payment experience for their customers.

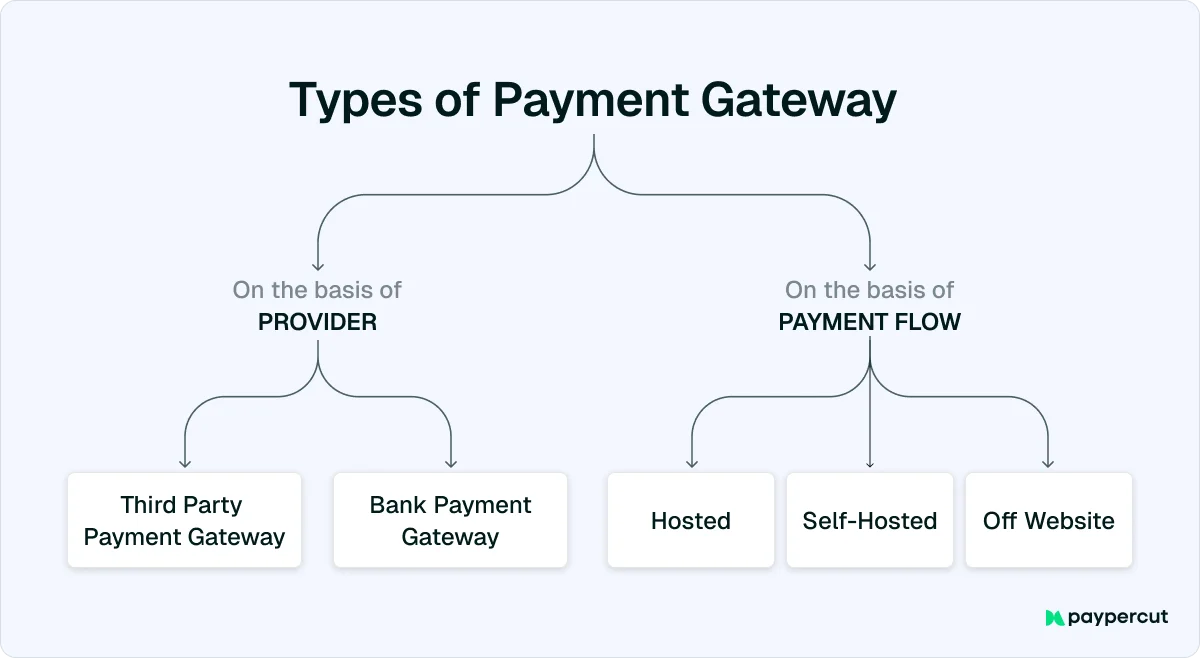

What is a payment gateway?

A payment gateway is a technology platform that facilitates electronic financial transactions between customers and businesses. It allows both online and in-person merchants to securely accept and process various payment methods, such as credit cards, debit cards, and digital wallets.

The payment gateway serves as a bridge connecting the customer, the business, and their respective banks. It ensures payments are processed quickly and securely, while typically charging a small fee per transaction.

How does a payment gateway work?

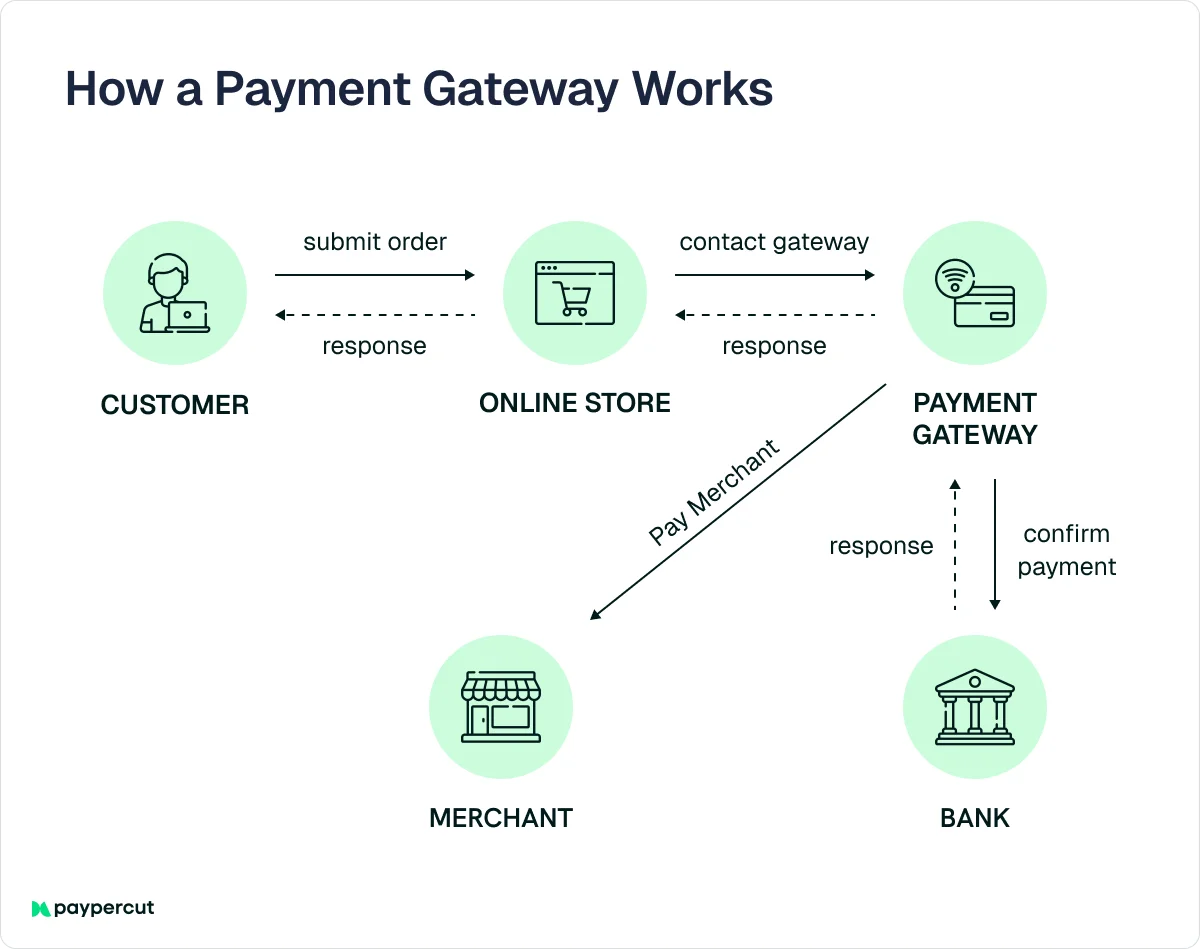

The payment gateway ensures every payment is safely authorized, verified, and completed within seconds.

Here’s how the process works:

1. Checkout and payment details

A customer selects the products or services they want to buy and proceeds to the checkout page. They enter their payment information, such as credit card details or digital wallet credentials.

2. Data encryption

After the payment details are submitted, the gateway encrypts the data using the SSL or TLS protocols. This encryption safeguards sensitive information from unauthorized access during transmission.

3. Transfer to the business server

The encrypted payment data is sent to the business’s server, where it is securely stored before being forwarded to the payment gateway. This step keeps the information protected before processing.

4. Forwarding to the processor

The payment gateway receives the encrypted transaction data and passes it to the payment processor and the acquiring bank. These financial institutions handle the technical aspects of processing the payment.

5. Transaction authorization

The acquiring bank sends the transaction information to the customer’s issuing bank or payment processor for verification. The issuing bank checks account details, confirms available funds, and validates the payment method.

6. Approval or decline

Once verification is complete, the issuing bank or processor either approves or declines the transaction. This response is sent back through the acquiring bank and payment gateway to the business’s server.

7. Transaction update

The payment gateway communicates the final transaction status—approved or declined—to the business’s website or app. If approved, the business fulfills the order. If declined, the customer is notified and can choose another payment method.

Payment Aggregator vs Payment Gateway: Key Differences

While both Payment Aggregators and Gateways enable digital transactions, their roles, regulatory responsibilities, and fund-handling mechanisms differ significantly.

1. Core function

The first key difference between these two lies in the specific roles they play in facilitating digital payments:

🔵 Payment Gateway

Primarily responsible for data transfer and payment authorization, a payment gateway ensures secure communication between the merchant’s checkout page and the acquiring bank.

It validates card or UPI details, transmits the information safely, and confirms whether a transaction is approved or declined.

🟠 Payment Aggregator

Acts as a comprehensive payments solution that goes beyond basic authorization. A payment aggregator not only onboards merchants but also collects payments, temporarily holds funds in a nodal account, and manages the final settlements.

It encompasses the core gateway function while adding critical financial, operational, and compliance layers to streamline the entire payment process.

2. Regulatory requirement

The second major difference between the two lies in their regulatory obligations and the extent of oversight they face from financial authorities.

🔵 Payment Gateway

Generally not directly regulated, as it does not handle or hold customer funds.

Its primary compliance responsibilities revolve around adhering to PCI-DSS guidelines, ensuring robust data encryption, and maintaining strict security standards to protect sensitive payment information.

🟠 Payment Aggregator

Subject to much stricter regulatory control, a payment aggregator must obtain authorization or licensing from financial regulators.

It is required to maintain designated nodal accounts, comply with KYC and AML norms, and follow defined settlement timelines to ensure transparency and accountability in fund management.

3. Merchant relationship and onboarding

Let’s explore how each model manages its relationship with merchants and facilitates their onboarding process:

🔵 Payment Gateway

A payment gateway requires merchants to maintain their own merchant account with an acquiring bank before accepting online payments.

This setup is generally preferred by established businesses with larger transaction volumes, as it offers greater control and potentially lower transaction costs once operational.

🟠 Payment Aggregator

A payment aggregator enables merchants to start accepting payments without a direct merchant account.

The aggregator handles the entire onboarding process, including KYC verification, compliance checks, and settlement management, making it a convenient choice for small and medium businesses seeking quick and simplified access to digital payments.

4. Fund flow and settlement

Another major difference lies in how funds move through each system and where settlement responsibilities are handled.

🔵 Payment Gateway

Funds are transferred directly from the customer’s issuing bank to the merchant’s acquiring bank account. The gateway itself never holds or manages money. It only facilitates the secure transmission of payment data between the parties involved.

🟠 Payment Aggregator

In this model, funds are first routed to the aggregator’s nodal or escrow account, where they are temporarily pooled before being disbursed to the merchant. Settlement takes place after proper reconciliation, ensuring accuracy, compliance, and transparency in the flow of funds.

5. Integration and services

The distinction here revolves around how each model integrates with merchant systems, supports payment functions, and delivers added-value services.

🔵 Payment Gateway

Primarily offers technical tools such as APIs, SDKs, and plug-ins to enable secure card processing and transaction authorization.

It is often integrated directly by large merchants or operates as part of a payment aggregator’s backend infrastructure to support seamless digital payment flows.

🟠 Payment Aggregator

Delivers an all-in-one platform that combines gateway capabilities with a unified dashboard for merchants.

It typically includes analytics, dispute management, refunds, subscription billing, and automated payouts, offering a comprehensive suite of services to simplify payment operations and enhance business efficiency.

6. Pricing and fees

Each model adopts a distinct pricing framework that balances transaction charges, setup costs, and the scope of included services.

🔵 Payment Gateway

Typically offers lower per-transaction fees since it focuses solely on processing and authorization. However, merchants may incur additional setup, integration, or maintenance costs, making it more suitable for established businesses that can manage upfront expenses.

🟠 Payment Aggregator

Generally charges a slightly higher Merchant Discount Rate (MDR) per transaction, as the pricing includes not only gateway services but also compliance management, fund settlement, and customer support.

Most aggregators, however, eliminate setup fees, providing a more accessible option for small and medium-sized merchants.

7. Risk & compliance responsibility

Risk management and regulatory compliance differ between the two models, particularly in how each handles financial exposure, data security, and adherence to legal obligations.

🔵 Payment Gateway

Carries minimal financial risk, as it does not handle or store customer funds. Its primary responsibility is ensuring transaction security through encryption, fraud prevention tools, and compliance with data protection standards such as PCI-DSS.

🟠 Payment Aggregator

A payment aggregator assumes greater operational and compliance responsibilities. It is accountable for fraud detection, handling chargebacks and refunds, and maintaining KYC and AML compliance records for both merchants and customers.

How to choose the right payment solution for your business

When deciding between a payment gateway and a payment aggregator, carefully evaluate the following factors, as the right choice can make a significant difference in how efficiently and securely your business handles payments.

- Business scale – Start by understanding the size and growth stage of your business.

Smaller businesses or startups often benefit from a payment aggregator due to its simplicity and quick setup, while larger enterprises may prefer a dedicated payment gateway for greater control and customization.

- Transaction volume – Analyze your expected monthly transaction volume to gauge cost efficiency.

High-volume businesses might find gateways more economical in the long run, while aggregators are often more cost-effective for businesses with lower or unpredictable transaction numbers.

- Integration needs – Consider how easily each option can integrate with your existing systems and platforms.

If your technical team has limited resources, an aggregator with ready-made plugins or APIs can simplify the process, whereas a gateway may require more development effort but offer deeper customization.

- Payment methods – Ensure the solution supports the payment methods your customers most frequently use, such as credit cards, digital wallets, or bank transfers. Providing multiple payment options not only improves the checkout experience but can also increase conversion rates.

- Security – Payment security should never be overlooked. Confirm that the provider adheres to strict security protocols and complies with PCI DSS to safeguard customer data and maintain your business’s credibility.

- Costs – Compare pricing models across different providers to understand the total cost of ownership. Look beyond basic transaction fees. Consider setup charges, monthly maintenance fees, and any hidden costs that could impact profitability over time.

- Customer Support – Choose a provider known for dependable and responsive customer service.

Having access to knowledgeable support, especially during integration or technical issues, can help prevent downtime and ensure a smooth experience for both your team and your customers.

Meet Paypercut – your localized payment partner

Choosing between a payment gateway and a payment aggregator ultimately depends on your business needs, scale, and technical setup.

But what if you could get all the benefits of both – secure processing, easy integration, and local payment methods – in one place?

That’s exactly what Paypercut offers!

If you’re a small or mid-sized business looking for a simple, localized way to accept payments and offer flexible options like Buy Now, Pay Later (BNPL), Paypercut is built for you.

Paypercut is a localized online payment stack created for businesses across Central and Eastern Europe.

With a single integration, you can accept cards (Visa, Mastercard), digital wallets (Apple Pay, Google Pay), and BNPL payments, all in your market’s currencies, payment methods, and onboarding requirements.

Here’s what Paypercut brings to your business:

- All-in-one payment platform – Manage card, wallet, and BNPL payments from one simple dashboard. Handle settlements in your local currency (BGN, RON, HUF, PLN, CZK, EUR, and more) without juggling multiple providers.

- Fast onboarding, no lock-ins – Start accepting payments quickly with no long-term contracts or hidden setup fees. Get verified, integrated, and ready to sell in just a few steps.

- Seamless integration options – Connect easily through our REST APIs or ready-made plugins for WooCommerce, OpenCart, and Shopify.

- Localized experience – Deliver checkout flows that speak your customers’ language and match their preferred payment habits. Everything is localized, from currency and language to compliance and settlement.

- BNPL aggregator – Access multiple Buy Now, Pay Later providers through one connection, boosting your approval rates and making cross-border selling effortless.

- Transparent merchant dashboard – Monitor all transactions, payouts, and fees in real time for full visibility and control.

- Friendly, human support – Get help from real people who understand your market and guide you through every step of setup and growth.

Join Paypercut today to get a localized partner that helps your business grow faster, sell smarter, and offer a better experience to every customer.