Customers don’t abandon checkout because your product is bad. They abandon because they can’t pay the way they want.

Cards are still the baseline, but they’re no longer enough. Wallets, BNPL, instant bank transfers, and local methods increasingly determine whether a purchase is completed or dropped.

Over 70% of carts are abandoned globally, and a meaningful share of those drop-offs comes from missing or unfamiliar payment options.

Choosing the right payment methods is no longer a technical decision. It’s a conversion decision.

This guide breaks down the most relevant payment methods in e-commerce today, what each solves, where it falls short, and how to decide which ones actually make sense for your business.

Key takeaways

- Payment cards remain the most popular e-commerce payment method.

European online shoppers still primarily use cards. Digital wallets come second, and they’re becoming more widespread. Modern solutions such as instant payments, BNPL, and cryptocurrency remain niche for most merchants despite their growing adoption.

- Each payment method comes with distinct tradeoffs.

Cards are universal but carry processing fees and chargeback risks. BNPL drives larger orders, but costs more and doesn’t make sense for low-margin products. Knowing when a method isn't the right fit is just as important as knowing when it is.

- Preferences for payment methods vary across demographics.

What works for a dropshipping enterprise in Bulgaria won't necessarily work for a small Greek business. Additionally, while most shoppers prefer cards, younger shoppers favor digital solutions. Research your customer base before committing to any setup.

- Accepting various payment methods is easy with Paypercut.

Managing multiple payment methods doesn't have to mean managing multiple providers, dashboards, and contracts. Paypercut consolidates all methods into a single integration, letting you scale across markets without rebuilding your checkout.

Most popular e-commerce payment methods

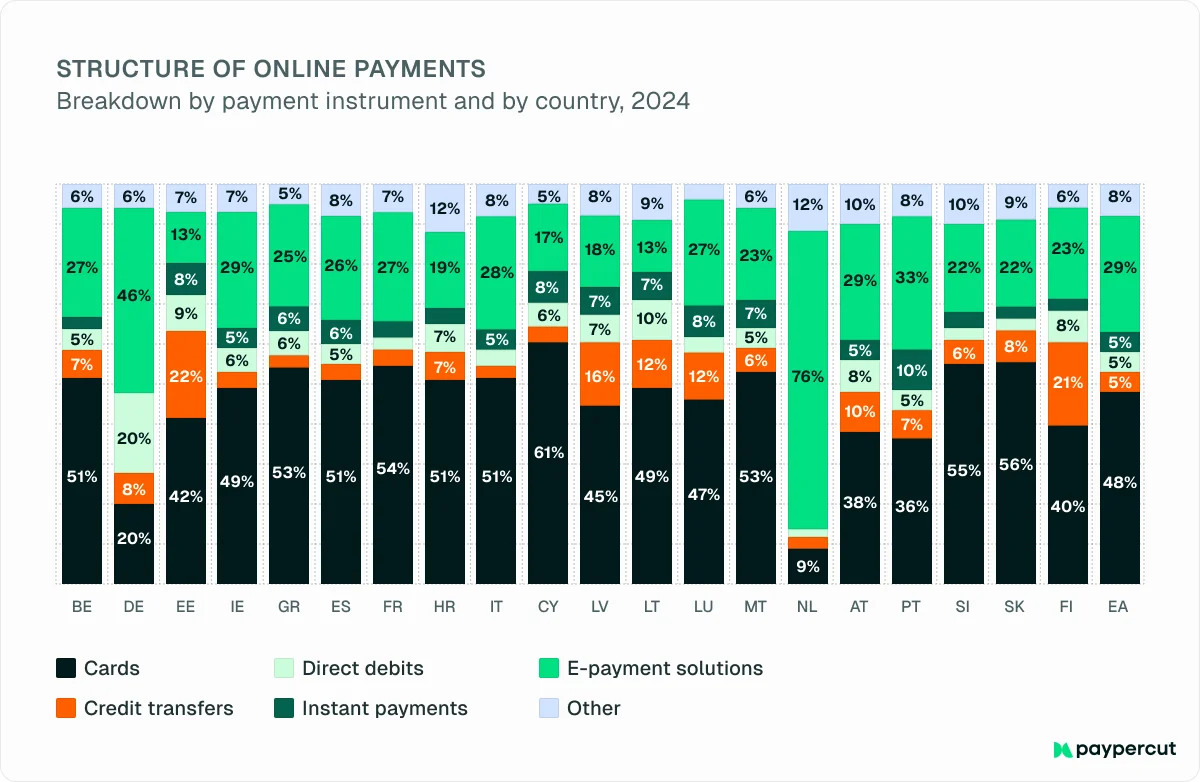

Here’s a list of online payment methods commonly used in 2024, based on the European Central Bank’s report:

The structure of online payments is similar across all 18 analyzed countries except in Germany and the Netherlands, where digital solutions outperformed cards.

Top 6 payment methods in e-commerce and when to offer them

Here’s an overview of the 6 best e-commerce payment methods and their key traits:

Here’s a quick decision guide:

- Start with cards + wallets → covers most users

- Add local methods → if entering a specific market (e.g., BLIK in Poland)

- Add BNPL → if average order value is €50+

- Add bank transfer/debit → if you run subscriptions or high-value orders

- Add COD → only in low-trust markets

1. Debit and credit cards

Card payments remain the most popular method for online commerce across Europe. Most consumers already own them and know how to use them. Most merchants already accept them. Additionally, card networks like Visa and Mastercard protect you and the consumer from fraud.

When a customer enters card details at checkout, your payment processor sends the information to the card network for authorization. Funds move from the customer's bank to yours, typically settling within a few business days.

On the downside, processing fees cut into margins, especially for lower-ticket items. In addition to standard card rates, you need to account for higher fees associated with cross-border transactions and commercial cards. Chargebacks may create additional expenses. Some customers abuse the dispute process, and even legitimate chargebacks require time to contest.

When to offer cards

- Always. If you accept nothing else, accept cards.

- You sell across borders, and local method coverage is uncertain.

When other methods are still necessary

- When average order value is low (under €15–20), processing fees take a disproportionate share of revenue. Offering alternative methods could result in significant cumulative savings.

- Cart abandonment can be high among mobile shoppers, and other methods, such as wallets, may convert better.

2. Digital wallets

Digital wallets store payment credentials on smartphones and authenticate purchases with biometrics or PINs. While cards may require consumers to enter 16-digit card numbers and CVV codes, wallets enable one-tap payments.

Wallets are also more secure because tokenization replaces actual card numbers during transactions, reducing fraud and authorization failures.

Usage of e-wallets today is higher among younger shoppers, but rates are climbing across age groups. The European mobile wallet market is projected to reach $31 billion by 2033, growing at 27% annually.

Apple Pay and Google Pay are available in most European markets, while local options such as BLIK in Poland and Viva Wallet in Greece dominate specific regions.

These geographical differences can pose a challenge. Supporting every option is often tedious and costly, as each wallet requires a separate integration, contract, and reconciliation process at month-end. Before you start offering wallets, research your specific market and pick the option based on local popularity.

When to offer digital wallets

- Your customer base skews younger or mobile-first. Wallet checkout consistently reduces friction on smartphones.

- You’re selling in markets with a dominant local wallet (BLIK in Poland, for example). Not supporting it means losing sales to competitors who do.

When wallets are not worth the investment

- Your customers primarily shop on desktop and save card details.

- Your target market has limited coverage of digital wallets.

3. Bank transfer

Bank transfers move funds directly between accounts, skipping card networks entirely. They're one of the oldest payment methods, and consumers across Europe still trust them for online purchases, especially for higher-value orders.

Two variations are especially common in e-commerce:

- Instant payments: Instant transfers process transactions in seconds, and thus provide a checkout experience similar to card payments. Adoption is growing fast. Over 62% of euro area consumers reported having access to instant payments in 2024, and 45% had already used them.

- Direct debit: Customers authorize you to automatically pull funds from their account according to a set schedule. This method is ideal for subscriptions and recurring billing. It lowers costs compared to card payments and provides more predictable cash flow with less manual follow-up.

Instant payments carry processing fees comparable to cards. Direct debit, while cheaper per transaction, comes with slower settlement times and higher chargeback risk.

SEPA has standardized direct debit across Europe, but setup and management can still be resource-intensive depending on your payment provider. You’ll need to collect, store, and update customer authorizations, and deal with failed pulls in case of insufficient accounts or closed accounts.

Small teams often find that this administrative overhead eats into the cost savings that made direct debit attractive in the first place.

When to offer bank transfers

- You provide subscriptions or recurring billing.

- Orders are generally high-value.

- Your target markets have strong payment infrastructure, so customers expect the option.

When to skip or deprioritize bank transfers

- Orders are usually one-time and low-value. The setup overhead isn’t justified.

- Your provider doesn’t handle mandate management reconciliation, and you don’t have the internal capacity to take them on.

- The target market sees low adoption rates. For example, the investment may not be worth it in Slovakia or Slovenia.

4. Buy Now, Pay Later (BNPL)

BNPL lets customers split a purchase into smaller installments. Most providers pay you the full amount upfront, in which case they take on the credit risk and collect payments from the customer over time.

Merchants who offer BNPL see ~30% higher conversion rates and ~20–40% higher average order values. Customers are more willing to complete a purchase and add more to their cart when the cost is spread across several payments.

The format appeals to younger shoppers who typically lack access to credit. It also performs well for higher-ticket items.

In Europe, BNPL use has grown at 25.5% annually since 2022, driven by new regulations and more banks entering the space. Since preferences vary across regions, offering multiple options is recommended, but this adds complexity.

On the cost side, BNPL fees range from 2% to 8%, running higher than standard card processing fees. Customer approval also depends on real-time credit checks, so not every shopper will qualify. A declined BNPL application mid-checkout often results in a lost sale entirely, since customers rarely switch to a different payment method after rejection.

When to offer BNPL

- You sell high-value products (€50–100).

- Your target audience is millennials or Gen Z.

- You sell electronics, furniture, or groceries—the categories that most commonly prompt the use of BNPL.

When not to include BNPL

- Your margins are below 15%, and fees of 4–8% consume most of the profit

- Order values are generally low, so most customers don’t need BNPL. The conversion lift is too low to justify the fees.

- You primarily sell product categories with high return rates, such as fashion. BNPL tends to increase impulse purchases, which customers return more often. When issuing a refund, BNPL providers usually keep the transaction fee they charge merchants.

Pro tip: Paypercut lets you offer multiple local BNPL providers through a single integration. It also acts as a provider when other options aren’t available. You can get paid upfront or enjoy a more cost-effective merchant-funded option.

5. Cash on delivery

Cash on delivery (COD) removes the trust barrier entirely, since buyers don't need to share financial details online, and only pay once they've seen the product.

Consumers’ fondness for cash remains strong across Europe today. 62% of consumers in the euro area consider it important or very important to have cash as a payment option, listing reasons such as privacy and better spending awareness. In markets where trust in online payments is still developing, such as Greece, COD can be the difference between a completed order and an abandoned cart.

Although cash payments don’t entail transaction fees, they still incur operational costs. COD increases the risk of refused deliveries, which means return shipping costs and tied-up inventory. Cash handling adds logistics complexity for couriers and delays your cash flow, since funds only arrive after successful delivery. \

When to offer COD

- You’re entering a market where trust in online payments is still developing.

- You sell physical products and want to reduce cart abandonment among first-time buyers who are unfamiliar with your brand.

- You primarily sell products with low return sensitivity, such as consumables, so customers are unlikely to refuse delivery.

When COD isn’t the right fit

- You operate across multiple markets and manage COD logistics in each.

- Your refused delivery rate exceeds 10–15%. At that point, the operational cost of returns, re-shipping, and inventory lock-up likely exceeds the revenue COD generates.

- You need fast cash flow. The settlement delay can strain working capital for a small business.

- You sell high-value items, so the risk of refused delivery is high.

6. Cryptocurrency

Crypto payments let customers pay with digital assets like Bitcoin or Ethereum. They’re processed through a payment gateway that converts them to fiat currency at checkout, which means you can avoid direct exposure to price swings.

The method appeals to a small but loyal segment of younger, tech-forward buyers who actively seek out merchants that accept crypto.

Still, adoption is rising among European consumers. The share of crypto holders in the euro area more than doubled between 2022 and 2024 (4% to 9%). Most people buy crypto as an investment, but its use for payments is picking up. The EU's Markets in Crypto-Assets (MiCA) regulation is expected to accelerate that shift by providing clearer rules for businesses and consumers.

For merchants, crypto offers lower transaction fees than cards, faster cross-border settlements, and no chargebacks.

However, there are many practical challenges to consider. For small e-commerce businesses, consumer adoption is still too low to justify implementing this method. Price volatility between transaction initiation and settlement can affect the value received, and tax reporting and accounting add administrative overhead that small businesses usually aren't set up to handle.

When crypto makes sense

- You sell digital goods or services to a tech-savvy, international audience.

- You’re in a niche where crypto enthusiasm is high, such as gaming, digital art, and tech hardware.

- Your margins are healthy enough to absorb the accounting and compliance overhead without significant strain.

When to hold off on crypto

- Your customer base isn’t there yet. The operational complexity isn’t justified by the handful of transactions you’d process.

- You don’t have accounting or tax expertise for crypto transactions. Getting this wrong can create regulatory problems that far outweigh the revenue.

- You sell physical products with frequent returns. Without a standardized dispute process, crypto refunds are manual and awkward for both sides.

Paypercut: One dashboard for all your payment methods

Payment preferences vary by region. Additionally, each payment method comes with its own providers, integration processes, and fee structures.

Trying to cater to as many customers as possible can quickly turn into a mess of separate contracts, scattered transaction data, and hours spent switching between platforms.

Paypercut lets you skip these problems without compromise. Instead of dozens of platforms, you can integrate with Paypercut once and get access to various payment methods, including:

- Cards

- Digital wallets

- Buy Now, Pay Later

- QR codes

- Linki do płatności

- Płatności cykliczne

Managing providers, payments, and revenue is simple with Paypercut’s all-in-one dashboard, whether your business is small or large.

Paypercut is also fully localized for Central and Eastern Europe and handles compliance and KYC onboarding, allowing you to complete these processes quickly online. Once set up, you can offer 12+ currencies, sell in 20+ European markets, and scale as needed.

Getting started doesn't require developer resources. Plugins for Shopify, WooCommerce, and OpenCart enable quick setup, and APIs are available for custom stores or different platforms. If you need assistance, Paypercut connects you with real experts to help you get up and running quickly.

Get started with Paypercut to offer the payment methods your customers expect, and help your e-commerce business grow.

Frequently asked questions

How do you choose payment methods for your e-commerce business?

Choosing payment methods starts with the outcome you want to improve.

If your goal is conversion, prioritize low-friction methods like cards, digital wallets, and BNPL. These reduce input effort and speed up checkout.

If you’re expanding into new markets, focus on locally dominant methods. For example, BLIK in Poland or region-specific wallets can significantly impact conversion.

If margins are tight, evaluate fees carefully. Some methods, like BNPL, increase conversion but come at a higher cost per transaction.

In practice, most merchants use a mix: cards as a baseline, wallets for mobile users, and one or two local methods depending on the market.

What is the most popular payment method for e-commerce?

At the moment, cards are the most popular e-commerce payment method in Europe and worldwide. Still, digital wallets are becoming more widespread. They’ve already surpassed cards in some parts of the world.

What are the best payment methods for cross-border e-commerce?

It depends on the region you’re selling to. Cards and e-wallets are leading methods worldwide, but some countries primarily use local options. For example, BLIK has been dominating the Polish market for years and will likely continue to do so.

The most effective approach is to research each target market individually and examine what local customers actually use, not just what's popular continent-wide. Consumer behavior, trust levels, and preferred checkout flows differ significantly even between neighboring countries.

In most cases, a combination of various methods is the optimal choice. For example, a mix of cards, wallets, and one or two locally relevant methods will cover the majority of your customers in any given market.

In addition to offering the right methods, focus on removing friction for cross-border buyers. For starters, display prices in local currency, provide checkout in the local language, and make the payment terms clear.

Pro tip: With Paypercut, your customers get a smooth checkout experience in the local language with all their favorite methods and providers. This minimizes drop-offs and improves conversions by 40%.