The way we pay for things is changing fast, and Buy Now, Pay Later (BNPL) is at the heart of that transformation.

What started as a simple checkout option has evolved into a global movement redefining how consumers spend and how businesses sell.

In 2026, BNPL is no longer just about deferred payments. It represents convenience, confidence, and financial control.

In this article, we’ll explore the key Buy Now, Pay Later trends that are redefining the future of retail and consumer finance.

Key Takeaways

BNPL is moving from trend to global standard

Buy Now, Pay Later has shifted from a niche fintech tool to a mainstream payment method, projected to exceed $560 billion in global transaction volume by 2026. Consumers love it for its flexibility, transparency, and ease of access, making it a staple in e-commerce checkouts worldwide.

Europe is a major growth hub for BNPL adoption

Europe now accounts for roughly a quarter of global BNPL revenues, with countries like Sweden, Germany, and France leading adoption. Central and Eastern Europe (CEE) is emerging as the next frontier, offering untapped potential for merchants to win new customers by integrating BNPL at checkout.

- BNPL is expanding into new sectors and channels

What began as a retail solution is now spreading to travel, healthcare, home improvement, and even in-store shopping through mobile wallets and virtual cards. Omnichannel BNPL users spend up to 72% more per transaction, showing the power of flexible payment options to boost sales and loyalty.

- Regulation and responsible lending are shaping the next phase

As BNPL matures, regulatory oversight is increasing across Europe under the new Consumer Credit Directive (CCD2). This brings higher standards for affordability checks and transparency, encouraging sustainable growth and consumer trust in BNPL providers.

- Merchants need unified solutions to stay competitive

With multiple BNPL providers, compliance rules, and integration challenges, businesses need a simpler way to manage it all. Paypercut solves this by connecting merchants to multiple BNPL options through one easy integration, helping you reach more customers, increase conversions, and scale across markets effortlessly.

The rapid global growth of BNPL

BNPL has grown from a small fintech option into a popular global payment method, changing the way people shop and manage their payments around the world.

Global market growth

The BNPL market is experiencing steady growth, driven by the expansion of digital commerce and consumers’ increasing preference for flexible payment options.

- The global BNPL market size, measured by total gross merchandise volume (GMV), is expected to reach $560.1 billion in 2026, reflecting a 13.7% annual increase.

- From 2021 to 2024, the industry experienced a strong 21.7% compound annual growth rate (CAGR), indicating rapid adoption across various markets.

- Growth is projected to moderate to around 10% CAGR between 2025 and 2030, indicating sustained global demand and a maturing market.

Rising global adoption

Increasingly, more consumers are opting for BNPL each year, drawn by its convenience, transparency, and ease of access.

- The global number of BNPL users is projected to surpass 900 million by 2027, up from 360 million in 2022 – a 157% increase over five years.

- Europe, Asia-Pacific, and Latin America are leading adoption, with Sweden, Australia, and the Nordics reaching double-digit shares of eCommerce payments.

Growth drivers

- E-commerce expansion: The continued rise of online and mobile shopping naturally supports BNPL as a preferred payment option, offering a fast and flexible checkout experience.

- Fintech integration: Modern APIs make it simple for merchants to embed BNPL directly into their payment systems, streamlining adoption and improving the customer journey.

- Evolving consumer preferences: More and more people are choosing interest-free installments and quick approvals because Buy Now, Pay Later feels simpler than traditional credit. Since the repayment terms are clear and smaller purchases don’t require hard credit checks, it comes across as an easy and transparent way to pay.

- Greater financial control: BNPL appeals to people who want flexibility and a clear view of their everyday spending. It helps them feel more confident and in control when making financial decisions.

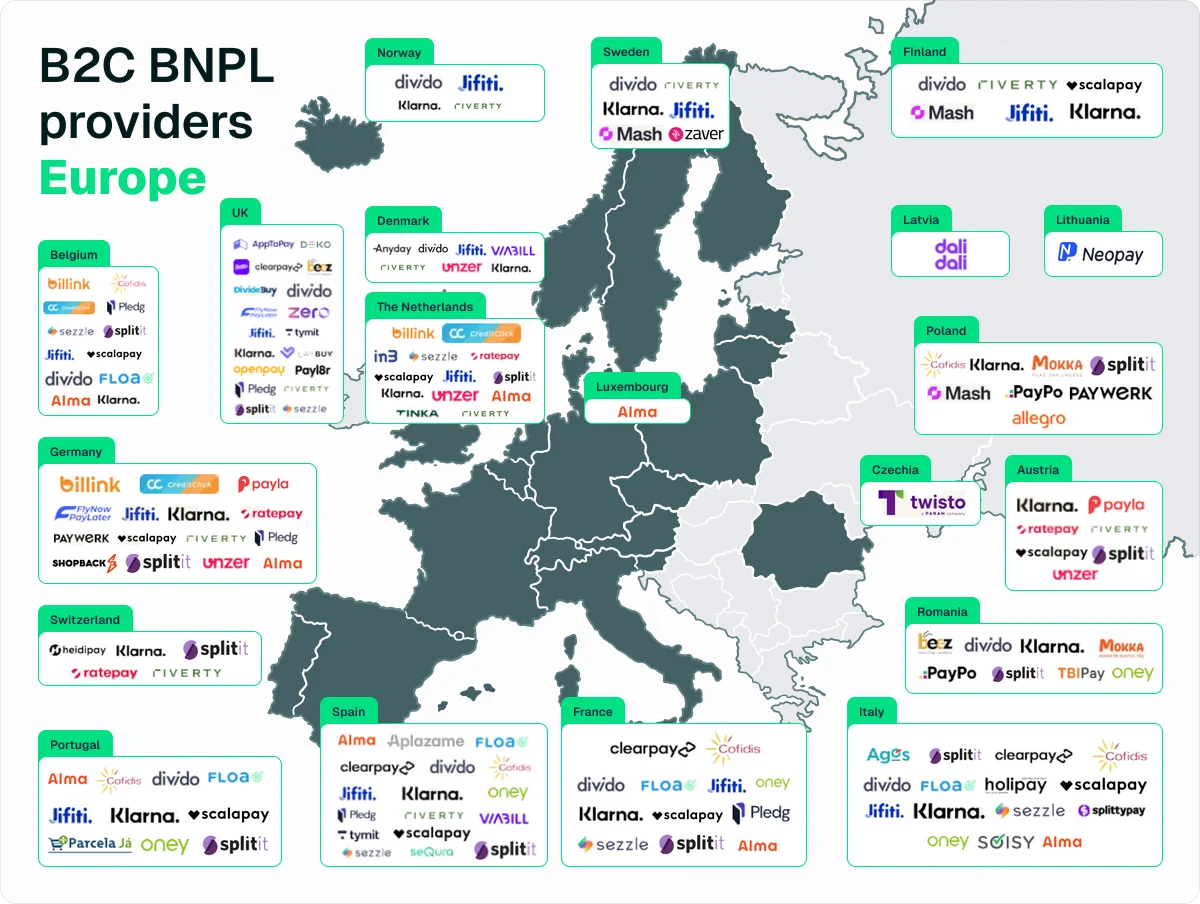

BNPL in Europe: On the rise across the continent

As consumers increasingly embrace flexibility and convenience, and as merchants seek ways to drive sales, BNPL has become one of the continent’s most dynamic payment trends.

Expanding market

BNPL is quickly becoming a key part of how people pay across Europe, gaining momentum in both well-established markets and those that are still growing.

- In 2024, Europe accounted for a quarter (25.9%) of global BNPL revenues, second only to Asia-Pacific.

- Total BNPL payments are expected to reach up to nearly $293.7 billion by 2030. At this pace, the European BNPL market is set to almost double in size within the next few years.

- Northern and Western Europe are leading the charge. Countries like Sweden, home to Klarna and other early innovators, have BNPL usage rates exceeding 23–24% of e-commerce transactions.

- Larger markets, such as Germany and France, are catching up quickly as consumers become more comfortable with flexible payment options.

- BNPL represents approximately 9% of all e-commerce transactions in Europe, meaning that nearly one in ten euros spent online utilizes a pay-later model. That share is expected to reach around 11% in 2025, and some projections go even higher, up to 14% within a few years.

.webp)

Central & Eastern Europe: The next growth frontier

While Central and Eastern Europe (CEE) is still in the early stages of BNPL adoption, it’s also where some of the most exciting growth is taking place.

- In most CEE markets, BNPL represents under 5% of e-commerce transactions, about half the European average. However, this gap underscores a significant opportunity for expansion as awareness grows and fintech providers scale their presence.

- Poland stands out as an early leader: about 64% of consumers there have used BNPL or installment options, and the market grew 181% year-on-year in 2022, reaching PLN 2.1 billion in financed purchases.

- Homegrown innovators such as PayPo, Twisto, and Allegro Pay are leading the charge, inspiring a wave of BNPL startups across Romania, the Czech Republic, and the Baltic states.

- For small businesses in CEE, these European trends signal that BNPL is becoming an expectation for many shoppers. Younger consumers across Europe (including CEE) increasingly look for BNPL at checkout as a standard option, much like they expect to see card payments or digital wallets.

Trends shaping the future of BNPL for 2026

New developments are continuously reshaping how “buy now, pay later” works and how it’s perceived. Here are some of the key trends in 2025 that are influencing the future of BNPL:

1. Expansion into new sectors

Buy Now, Pay Later (BNPL) services first took off in retail and e-commerce, covering fashion, electronics, and online shopping. But in 2025, BNPL has moved far beyond traditional retail into a variety of new industries, such as:

- Travel bookings – Airlines and travel platforms now let customers split the cost of flights, hotels, or full vacation packages into manageable installments.

- Healthcare and dental procedures – Medical and fintech companies offer flexible payment plans for elective or cosmetic treatments, easing financial pressure on patients.

- Veterinary care – Pet owners can spread out the cost of unexpected or routine vet bills.

- Home improvement projects – From renovations to new appliances, homeowners can finance upgrades more easily.

2. In-store and omnichannel BNPL

Major BNPL providers are extending their reach beyond online checkouts, creating seamless payment experiences across both digital and physical shopping environments.

Today, shoppers can use BNPL in-store through:

- Virtual cards or one-time numbers – Providers like Klarna generate unique card details that work just like a credit or debit card at checkout.

- Mobile wallet integrations – BNPL options can now be added to Apple Pay or Google Pay, allowing customers to simply tap their phone in a boutique or retail store and pay later.

Studies show that omnichannel BNPL users spend about 72% more per transaction than standard online shoppers.

3. Consolidation and partnerships

The BNPL market is maturing, marked by consolidation, strategic partnerships, and ecosystem integration. Key trends include:

- Mergers and acquisitions – Larger players are acquiring smaller competitors to strengthen their position. In Central and Eastern Europe, for instance, Czech-based Twisto was acquired first by Australia’s Zip Co and later by Turkey’s Param.

- Strategic partnerships – BNPL providers are partnering with e-commerce platforms (such as Shopify and WooCommerce), telecommunications companies, and other brands to expand their reach and improve integration.

- Aggregator platforms – New BNPL aggregators, such as Paypercut, allow merchants to connect with multiple BNPL providers through a single integration, simplifying adoption and boosting flexibility.

4. Consumer debt and responsible lending focus

With BNPL’s explosive growth has come greater scrutiny from regulators and consumer advocates concerned about rising debt levels.

- Late payments on the rise – Globally, an estimated 34–41% of BNPL users reported making at least one late payment in the past year, and among Gen Z users, that figure climbs to around 51%. These delays often result in late fees and can signal growing financial strain among younger or less experienced borrowers.

- Shift toward responsible lending – As BNPL becomes more mainstream, both regulators and providers are putting a stronger focus on responsible lending. They want to make sure customers understand what they’re agreeing to, can afford their payments, and aren’t pushed into taking on too much ‘easy’ credit.

5. Regulatory changes on the horizon

The growing focus on responsible lending is now being codified into law. As BNPL expands, regulators across Europe are stepping in to ensure the industry develops sustainably.

Under the updated Consumer Credit Directive (CCD2), expected to be implemented by the end of 2025, BNPL will formally fall under consumer credit regulation, introducing requirements for affordability checks, transparent terms, and potential caps on late fees or interest.

At the national level, some countries are already moving ahead. For example, Poland’s 2023 anti-usury law amendments require BNPL providers to report to the financial regulator and comply with interest caps, just like banks.

6. Greater emphasis on financial education

Alongside new regulations, BNPL providers are placing greater focus on consumer education and financial awareness. The goal is to promote responsible use and position BNPL as a smart budgeting tool rather than a gateway to overspending.

- In-app guidance – Many BNPL apps now include spending reminders, payment notifications, and personalized insights to help users manage repayments more effectively.

- Partnerships for financial wellness – Some providers are collaborating with financial literacy programs and fintech education platforms to help consumers build better money habits.

- Responsible branding – Expect more BNPL companies to market themselves as “safe and transparent” providers, highlighting features like spending limits, hardship policies, and flexible repayment options.

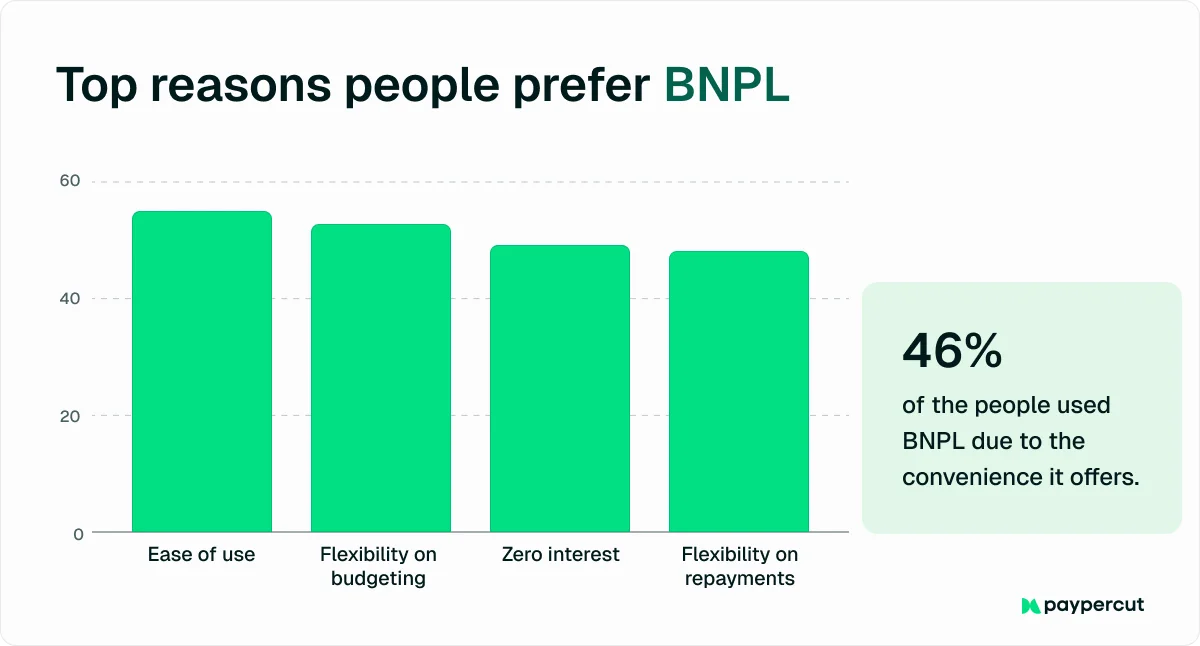

Inside the consumer mindset: Why shoppers love BNPL

Buy Now, Pay Later (BNPL) has grown rapidly across Europe because it fits today’s shopper mindset: convenience, transparency, and better control over spending.

Here’s what drives the appeal:

- Convenience first: BNPL allows shoppers to split payments into manageable chunks instantly, with no lengthy applications or credit checks required. The process feels effortless, with just a few clicks at checkout and a clear repayment plan in place.

- Interest-free advantage: Many European BNPL services offer short-term, interest-free payments if made on time. Compared to traditional credit cards with high APRs, it feels like a smarter, more affordable way to buy.

- Budget-friendly psychology: Paying €50 now instead of €200 upfront makes big or discretionary purchases feel less daunting. This small-step approach makes “add to cart” decisions easier.

- Young user dominance: Millennials and Gen Z are the core BNPL audience, especially those aged 25–34. They’re digital natives who prefer managing payments through apps rather than traditional credit systems.

- Control and transparency: BNPL providers clearly display terms like “4 payments of €25, no fees,” giving shoppers full visibility. This upfront clarity helps them plan spending and avoid surprises.

- Changing financial attitudes: Younger Europeans are wary of long-term debt and see BNPL as short-term budgeting rather than borrowing.

- Economic relief: With the rising cost of living, spreading payments across paychecks helps maintain flexibility. What began as a pandemic-era habit has evolved into a lasting spending preference.

Meet Paypercut: One platform to manage every BNPL option

As the BNPL market continues to evolve, merchants across Central and Eastern Europe are seeking smarter, simpler ways to offer flexible payments without juggling multiple integrations or providers. This is where Paypercut comes in.

Paypercut helps small and mid-sized businesses accept online payments across cards, digital wallets, QR codes, and multiple BNPL providers through a single integration.

As the first BNPL aggregator in Central and Eastern Europe, Paypercut connects you to multiple trusted BNPL providers at once, helping you reach more customers, boost approval rates, and scale effortlessly across borders.

With no setup fees, no lock-in contracts, and human-first support, Paypercut makes it easy for merchants to start offering BNPL in days, while keeping full control over their cash flow.

What Paypercut provides you with:

🟢 One integration, multiple BNPL options – Connect with several BNPL providers instantly through a single API or plugin, enhancing approval rates and offering greater payment flexibility for your customers.

🟢 Localized payments and settlements – Operate smoothly across Bulgaria, Greece, Romania, Czechia, and beyond with local currency settlements that minimize foreign exchange risk.

🟢 Zero lock-in, pay-as-you-go model – No setup fees or contracts, you only pay a small percentage per transaction.

🟢 Merchant-funded BNPL capabilities – Offer installment plans even in markets without local BNPL providers, while retaining complete control over risk and approval criteria.

🟢 Partner revenue opportunities – Generate additional income by referring or onboarding new merchants through Paypercut’s partnership program.

🟢 Personalized support and effortless setup – Benefit from dedicated onboarding assistance, intuitive dashboards, and ready-to-use plugins for WooCommerce, OpenCart, and Shopify.

Get started today to bring simple, flexible BNPL payments to your store.