Are you looking for a Buy Now Pay Later (BNPL) provider to boost your sales and give your customers more flexibility at checkout?

In 2026, the BNPL market in Europe is expected to reach approximately US$191.3 billion, growing at an annual rate of roughly 12.4%, with more merchants than ever incorporating it as a standard payment method.

However, when choosing a provider, it’s important to look beyond the big names and consider factors like fees, risk management, integration, and customer support.

In this article, we’ll guide you through how to choose a BNPL provider that truly fits your business needs and helps you deliver a seamless payment experience for your customers.

Key Takeaways

- Choosing the right BNPL provider directly impacts growth and customer trust

A strong BNPL partner can increase conversions, raise average order value (AOV), and enhance loyalty by making payments easier and more transparent for customers.

- Evaluate providers for business fit, reliability, and flexibility

Look for BNPL partners that understand your industry, support both online and in-store transactions, and offer adaptable payment terms suited to your order sizes and customer base.

- Implementation ease and support matter for long-term success

The ideal BNPL solution should integrate smoothly with your existing systems, whether through APIs, plug-ins, or embedded checkout tools. Access to strong technical documentation and responsive support accelerates deployment and reduces complexity.

- Transparency and compliance protect your reputation and profits

Trusted providers clearly communicate fees, maintain regulatory compliance (e.g., PCI DSS, GDPR), and use advanced fraud prevention tools—ensuring both your business and your customers are protected.

- Paypercut simplifies BNPL with a smarter, all-in-one solution

Instead of juggling multiple providers, Paypercut connects you to several BNPL options through one integration. This means higher approval rates, broader customer coverage, and one easy-to-manage dashboard for all payments.

Benefits of choosing the right BNPL provider

Here are some of the key benefits of choosing the right BNPL provider:

- Higher conversion rates – A trustworthy BNPL option reduces checkout friction. Transparent and flexible payment choices encourage customers to complete their purchases, lowering cart abandonment and boosting sales.

- Increased Average Order Value (AOV) – Flexible installment options give customers confidence to spend more per order, often leading to noticeable lifts in AOV.

- Stronger customer loyalty – A smooth repayment experience builds trust and satisfaction, encouraging repeat purchases and long-term customer relationships.

- Improved cash flow – Even though customers pay over time, most BNPL providers settle with merchants quickly, helping maintain healthy cash flow and operational stability.

- Reduced operational risk – Providers with strong fraud prevention, real-time risk scoring, and compliance tools help protect your business from financial and regulatory exposure.

- Valuable customer insights – Access to detailed analytics on customer behavior, repayment trends, and spending patterns supports smarter marketing and merchandising decisions.

- Enhanced brand perception – Partnering with a reputable BNPL provider reinforces your image as modern, flexible, and customer-focused, strengthening trust and brand equity.

Selecting the right BNPL provider is a strategic decision that can directly influence your sales performance, customer satisfaction, and brand reputation.

Factors to consider when choosing a BNPL provider

Selecting the right BNPL partner requires balancing customer experience, risk management, and business performance. The following factors will help you evaluate providers strategically and choose one that delivers long-term value.

1. Make sure it’s fit for your business

Different industries, transaction types, and customer journeys come with unique challenges and expectations. Choosing a provider that understands these nuances and offers flexible, tailored solutions is key to long-term success.

Here are some essential elements to consider:

- Multichannel support – Choose a BNPL provider that operates seamlessly across both online and offline channels. Whether your customers are shopping via your e-commerce site, mobile app, or in-store, the experience should feel consistent and effortless.

- Customizable transaction management – Look for providers that support order modifications, price adjustments, and approval workflows when needed. This flexibility helps businesses manage complex orders and maintain transparency with their customers.

- Flexible payment terms for all order sizes – The ideal provider should accommodate both small purchases and large transactions with options for installments or deferred payments, helping customers manage their budgets while maintaining healthy cash flow for your business.

2. Reputation and reliability

Partnering with a trusted, well-established provider helps ensure that every transaction is handled securely, smoothly, and transparently, protecting both your business and your customers.

A provider’s credibility can be assessed through several key indicators:

Service track record

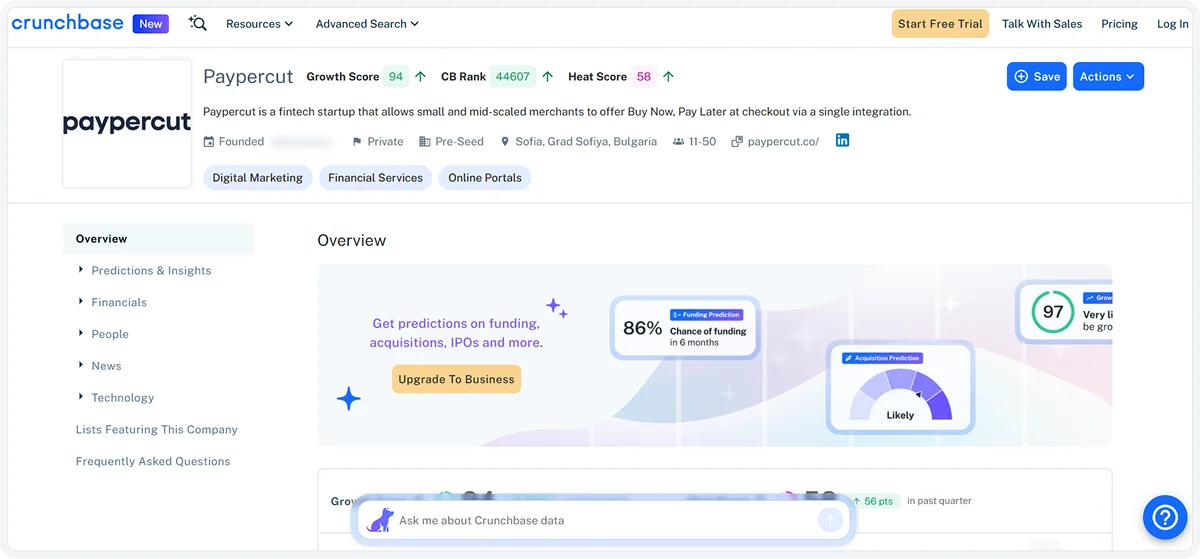

Review how long the provider has been operating, the volume of merchants and consumers they serve, and their historical performance in handling disputes or failed payments.

Visit the provider’s website for case studies and annual reports, search for company profiles on sites like Crunchbase or LinkedIn, and review any media coverage or industry analyses that discuss their growth or performance.

Customer feedback

Reviews and testimonials from other merchants and end-users can offer valuable insights into the provider’s real-world reliability and service quality.

Consider third-party review platforms such as Trustpilot, G2, or Capterra, along with app store ratings and merchant community forums. Reading both positive and negative reviews can reveal patterns in service and support quality.

Financial backing and partnerships

Strong investor support, recognized brand partnerships, or regulated financial institution backing often indicate long-term stability and operational integrity.

Check for press releases, funding announcements on TechCrunch or PitchBook, and verify any banking or retail partnerships through official partner websites.

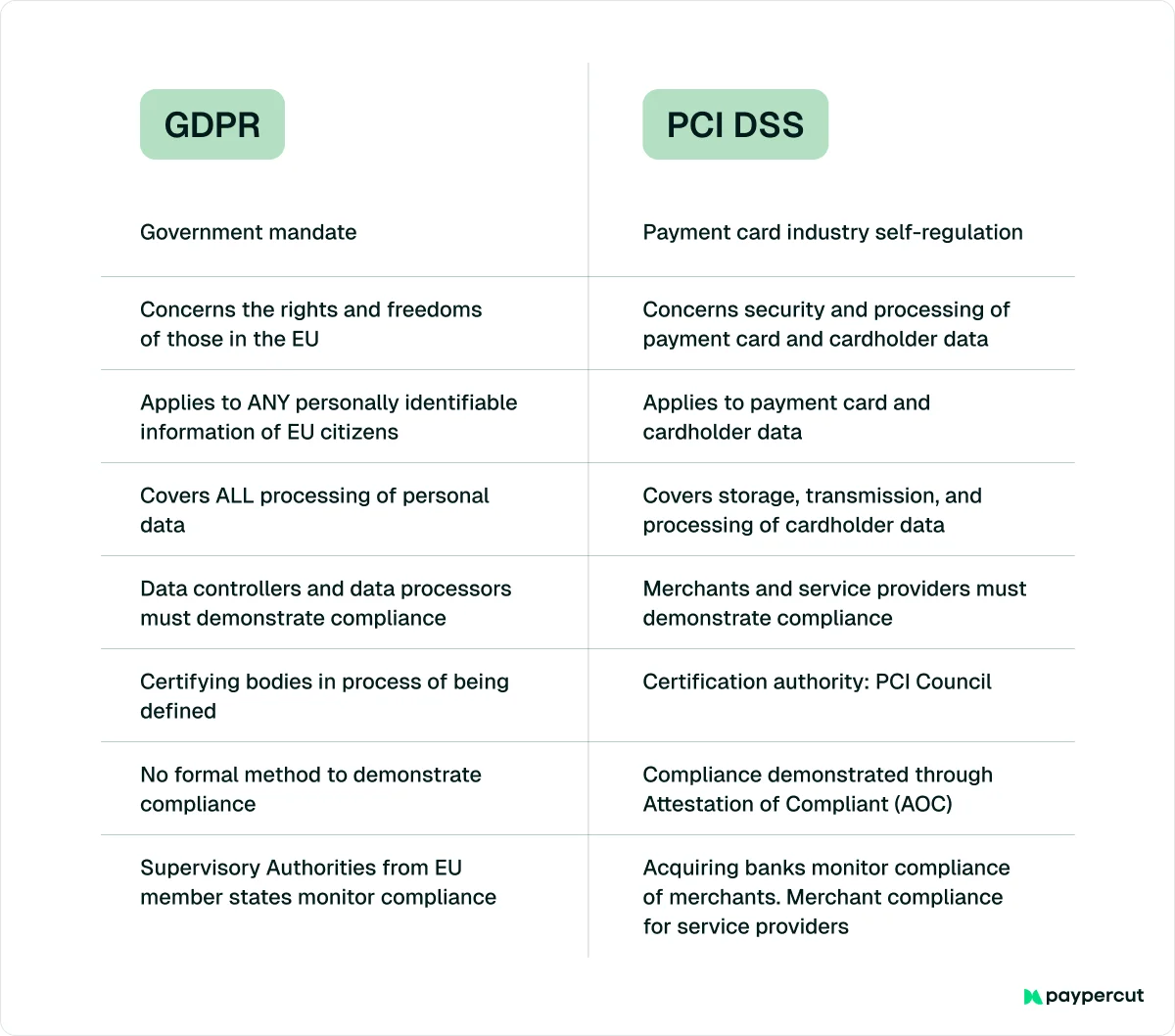

Regulatory compliance and certifications:

Ensure the provider adheres to relevant financial regulations and data protection standards, such as PCI DSS, GDPR, or local consumer credit laws.

Review disclosures on the provider’s website, confirm licenses on financial regulatory authority websites, and look for public compliance statements or audit certifications.

3. Ease of implementation and integration

A BNPL solution should be easy to implement and integrate into your existing systems. The smoother the setup, the faster you can start offering flexible payment options to your customers.

Look for providers that offer flexible integration paths and robust implementation support:

- Direct API integration – Connect directly through well-documented REST APIs for full customization, automation, and control over the customer journey.

- Embedded checkout or iFrame solutions – Seamlessly integrate BNPL functionality into your website or checkout flow with minimal development effort, ensuring a smooth and consistent user experience.

- Plug-ins and extensions – If you use popular e-commerce or CMS platforms (like Shopify, Magento, or WooCommerce), choose a provider that offers ready-made plug-ins for quick, low-code deployment.

- Analytics and dashboards – A comprehensive merchant portal or extranet lets you track transactions, monitor performance, and gain valuable insights in real time.

- Technical support and documentation – Look for providers that offer comprehensive developer documentation, sandbox environments, and responsive technical support.

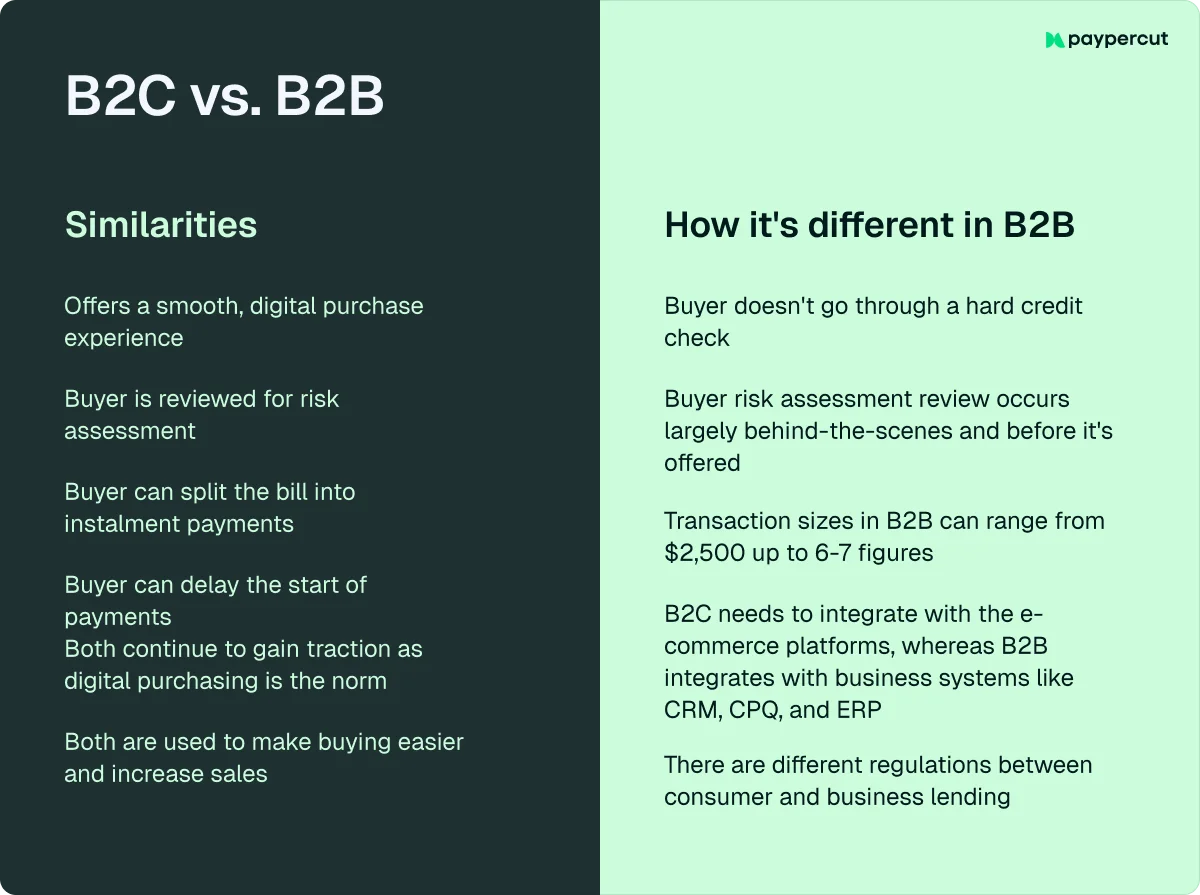

4. Flexibility in payment terms

A BNPL provider should offer customizable payment structures that align with your industry, transaction size, and customer base. Flexibility in terms helps you improve conversion rates, manage cash flow, and meet diverse buyer needs.

Look for providers that support adaptable payment options for different business models:

- B2C flexibility – Offer installment plans (e.g., 3, 6, or 12 months) to make higher-value purchases more accessible and boost conversion rates for consumer goods.

- B2B flexibility – Provide extended payment terms (e.g., 30, 60, or 90 days) to support wholesale buyers and SMEs with longer cash flow cycles.

5. Fees and Revenue-sharing models

A BNPL provider’s pricing structure has a direct impact on your profit margins and overall ROI. Choosing one with transparent, flexible fee models helps ensure long-term financial sustainability for your business.

Focus on the following aspects when comparing providers:

- B2C fee models – Transaction fees typically range between 2% and 3.5%, depending on factors like order value, risk level, and transaction volume. Seek providers that offer tiered or volume-based pricing to lower costs as your business scales.

- B2B fee models – Fees often vary based on invoice size, payment terms, and credit risk. Choose providers that offer transparent pricing and flexibility to accommodate larger invoices or longer repayment windows.

- Revenue-sharing opportunities – Some BNPL providers offer commission or revenue-sharing models, allowing you to earn a percentage of financing income or referral fees.

- Transparency and predictability – Ensure the provider clearly communicates all merchant-facing fees and deductions, such as transaction or platform fees, to avoid unexpected costs.

Below is a table with some common BNPL provider fees:

6. Shopping experience

A well-designed BNPL solution should enhance the entire purchasing journey, making payments simple, intuitive, and trustworthy. The smoother and more transparent the process, the higher the likelihood of repeat purchases and customer loyalty.

Here’s what today’s customers expect, and what to look for in a provider to meet those needs:

- Clarity and transparency – Customers expect clear, upfront information about payment terms, schedules, fees, and any potential charges.

- Credit protection – They want reassurance that using BNPL won’t negatively impact their credit score or borrowing history.

- Responsible spending support – Many expect features that help them manage repayments easily and avoid overspending.

- Data privacy and security – Shoppers want confidence that their personal and financial information is handled safely and responsibly.

- Fair and efficient dispute handling – Customers anticipate quick, transparent resolution of billing issues, refunds, or payment disputes.

- Flexibility and convenience – They appreciate reminders, flexible repayment options, and the ability to track or manage their payments effortlessly.

- Responsive customer support – Reliable, accessible support channels that allow customers to reach help quickly whenever they need it.

Global vs. Local BNPL provider

As BNPL continues to grow worldwide, businesses must decide whether to partner with a global provider or a local market specialist.

Each choice brings its own mix of benefits and trade-offs, depending on your company’s size, target audience, and expansion goals.

1. Global BNPL providers

Global BNPL leaders operate across multiple regions and currencies. Their solutions are designed for merchants seeking consistency, scalability, and a unified customer experience across international markets.

🟢 Key advantages:

- Wider reach and brand recognition – Global providers often have large existing customer bases, helping merchants attract international shoppers and increase conversion rates in cross-border sales.

- Streamlined operations – A single integration can unlock access to multiple countries, reducing the need for separate contracts or technical setups per region.

- Advanced technology and support – Large-scale providers usually offer mature APIs, robust fraud prevention tools, and strong infrastructure to handle high transaction volumes.

- Cross-market analytics – Centralized data and reporting make it easier to monitor performance, repayment trends, and customer behavior across regions.

🔴 Potential challenges:

- Less localization – Global platforms may lack a deep understanding of local payment habits, regulations, or language nuances.

- Higher costs – Their premium infrastructure and brand power sometimes translate to higher transaction fees or stricter contract terms.

- Limited flexibility – Standardized global frameworks may leave less room for customization or regional adjustments.

2. Local BNPL providers

Local BNPL providers, often regional fintechs or bank-backed solutions, focus on serving specific countries or territories. They typically design their offerings around local consumer preferences, regulatory requirements, and merchant needs within their market.

🟢 Key advantages:

- Deeper local insight – Local providers understand consumer behavior, purchasing trends, and payment expectations unique to each market.

- Regulatory alignment – They are often better equipped to navigate domestic compliance, credit, and data protection laws.

- Localized customer experience – Support in local languages, culturally adapted communication, and payment schedules aligned with local pay cycles enhance customer trust.

- Competitive pricing – Local providers may offer lower fees or more flexible contract terms to attract merchants in their region.

🔴 Potential challenges:

- Limited geographic coverage – Expanding into new markets may require integrating multiple providers, which complicates operations and reporting.

- Variable technology maturity – Some local providers may lack the scale or advanced technical capabilities of global players.

- Fragmented analytics – Managing multiple systems and data sources can make performance tracking more complex.

Paypercut: The smarter way to offer BNPL

Most merchants only work with one BNPL provider. This limitation affects their approval rates and coverage, as each provider employs different risk models, operates in different regions, and targets different customer segments. When one declines a customer, the sale is often lost.

Adding more BNPL providers can help address this issue, but managing separate integrations, contracts, and settlement processes quickly becomes complicated and time-consuming.

That’s where Paypercut offers a smarter solution.

As the first BNPL aggregator in Central and Eastern Europe, Paypercut connects you with multiple BNPL providers through one simple integration. This setup ensures broader coverage and higher approval rates – if one provider declines a transaction, another can step in to complete it.

The result? More completed purchases, higher approval rates, and a smoother experience for both you and your customers.

But Paypercut goes beyond BNPL. It’s an all-in-one, localized payment platform built for small and mid-sized businesses, offering card payments, digital wallets, and instalment options in one place, with no lock-in contracts and transparent pay-as-you-go pricing.

Here’s why merchants across the region choose Paypercut:

- All-in-one payment platform – Manage BNPL, card, and digital wallet payments from a single dashboard. Get local settlements in your currency (BGN, RON, HUF, PLN, CZK, EUR, and more).

- Fast onboarding, zero hassle – Get started in minutes, with simple integration options via API or ready-made plugins for WooCommerce, OpenCart, and Shopify and more.

- Localized experience – Offer payments in local currencies and languages, with checkout flows tailored to your market’s habits and regulations.

- Recurring and subscription payments – Automate billing for memberships or repeat services to save time and keep revenue flowing.

- Clear merchant dashboard – Track payments, payouts, and performance in real time for full transparency.

- Built for SMBs – Friendly onboarding support, clear documentation, and real people to guide you at every step.

Get started with Paypercut today and connect to multiple BNPL providers through one simple integration!

FAQs:

1. How can I tell if a BNPL provider is trustworthy?

Look for clear regulatory compliance (e.g., PCI DSS, GDPR), transparent fee structures, strong security measures, positive merchant reviews, and reliable customer support. Checking case studies and financial backers can also indicate credibility.

2. What are the risks of offering BNPL as a merchant?

The main risks involve potential chargebacks, disputes, or dependency on a single provider. Choosing a regulated and transparent BNPL partner helps minimize financial, operational, and reputational risk.

3. How do BNPL providers handle fraud and late payments?

Reputable providers use real-time risk scoring, identity verification, and automated fraud detection tools. They typically assume repayment risk, shielding merchants from losses due to customer defaults.

4. What metrics should I track after implementing BNPL?

Monitor conversion rates, average order value (AOV), repayment performance, customer acquisition cost (CAC), and repeat purchase rate. Most BNPL providers offer dashboards and analytics tools to help you measure ROI effectively.