Europe’s e-commerce market is already huge and still expanding, with revenues moving toward €770 billion in 2026. That puts growth at around 8.5%, which is higher than the rate in the Americas.

The growth of the European e-commerce market is driven by strong digital infrastructure, high internet penetration, and a steadily growing base of online shoppers, with 77% of internet users buying goods or services online in 2024.

These conditions make Europe a highly favorable market for selling online, as long as you have the right payment setup in place.

That’s where the payment service provider vs. payment gateway choice comes in.

Both help you accept digital payments, but they come with different trade-offs in cost, control, and operational effort.

This guide helps you understand those trade-offs and ultimately decide which setup makes more sense for your business.

Key takeaways

- PSPs handle everything, gateways handle one step

A payment service provider (PSP) covers the full payment flow, from checkout to payout. A payment gateway only handles the secure transfer of data, so you need additional providers to complete the process. - Your setup choice directly affects complexity and time to launch

PSPs are faster to implement because everything is bundled into one integration. Gateway setups take longer since you need to connect and manage multiple components like processors, fraud tools, and merchant accounts. - Control vs. simplicity is the core trade-off

Gateways give you more control over routing, fees, and payment flows, which matters at scale. PSPs prioritize simplicity with predefined setups, which works better for most SMBs early on. - Costs look simple at first, but change as you grow

PSP pricing is easier to understand with one bundled fee. Gateway setups are more complex but allow cost optimization across providers, which becomes important at higher volumes. - There’s a middle ground if you want both simplicity and flexibility

If you want to avoid managing multiple providers but still need flexibility across markets and payment methods, a solution like Paypercut gives you one integration for cards, wallets, and BNPL, with local payment logic built in and no heavy setup required.

What is a payment service provider?

A payment service provider (PSP) is a company that lets you accept online payments without having to set up and manage all the pieces yourself.

Essentially, a PSP acts as the middle layer between your business, your customer, and the banks involved in the transaction.

Instead of connecting to each part separately, you integrate once with the PSP, and it handles the rest.

How does a payment service provider work?

A payment service provider handles the full payment flow for you, connecting all the parties involved and managing the communication between them.

In practice, it looks like this:

- Customer enters payment details: At checkout, the customer selects a payment method and submits their details.

- PSP captures and sends the payment request: The PSP securely collects the data and forwards it to the relevant financial partners.

- Banks and card networks process the transaction: The request goes through card networks to the customer’s bank, which checks available funds and runs basic fraud and security checks before approving or declining the payment.

- Approval or decline is returned: The customer’s bank sends the decision back through the same chain to the PSP.

- You get the result instantly: The PSP shows the result at checkout (payment successful or failed).

- Funds are settled to your account: If approved, the PSP arranges for the money to be transferred to your merchant account and paid out to you.

The pros and cons of payment service providers

Pros

- Simple setup: You can start accepting payments quickly without setting up separate bank or processing relationships.

- All-in-one solution: Payments, settlement, reporting, and basic fraud tools are handled in one place.

- Multiple payment methods: You can offer cards, wallets, and local payment methods through a single integration.

- Easier international expansion: Many PSPs support multiple currencies and local payment options out of the box.

- Built-in compliance and security: The PSP handles many of the regulatory and security requirements for you.

- Centralized reporting: You get one dashboard to track transactions, payouts, and performance.

Cons

- Higher costs at scale: Per-transaction fees can become expensive as your volume grows.

- Less flexibility: Customizing payment flows or routing transactions is often restricted.

- Payout and settlement constraints: Timing and structure of payouts are defined by the PSP, not by you.

What is a payment gateway?

A payment gateway is the digital equivalent of a card terminal, focused on securely transferring payment data from your checkout to the payment processor and returning the result to your site.

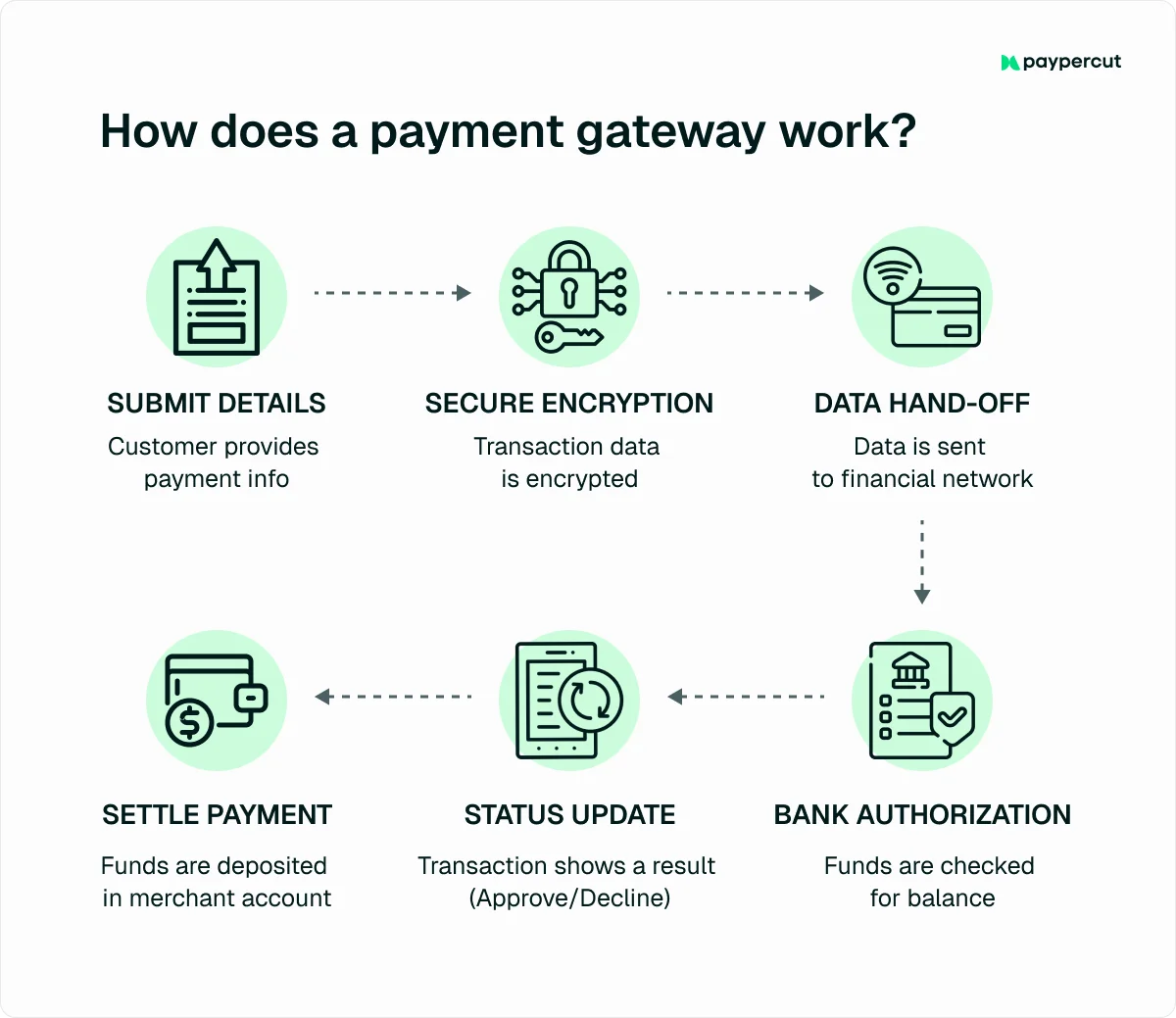

How does a payment gateway work?

A payment gateway sits between your checkout and the rest of the payment system, handling the secure exchange of data and returning a result in seconds.

The process looks like this:

- Customer enters payment details: The customer fills in card or wallet information at checkout.

- Gateway encrypts the data: The payment details are secured so they can’t be intercepted.

- Data is sent to the processor or acquiring bank: The gateway forwards the encrypted information to the next step in the payment chain.

- Authorization is requested from the customer’s bank: The transaction is checked via card networks and the issuing bank.

- Approval or decline is returned: The result is sent back through the gateway to your checkout.

- Transaction moves to settlement: If approved, the payment is passed on for processing and payout (handled outside the gateway).

The pros and cons of payment gateways

Pros

- More control over your setup: You can choose your own acquirer, processor, and payment flow.

- Flexible integrations: It works well with custom-built systems and existing banking relationships.

- Lower costs at scale: Fees can be optimized by negotiating directly with providers.

- Custom routing options: You can direct transactions based on cost, geography, or performance.

- Strong security layer: It handles encryption and secure data transmission at checkout.

Cons

- More complex setup: You need to connect and manage multiple providers yourself.

- A need for a merchant account: You must arrange your own acquiring setup before accepting payments.

- More responsibility for compliance: You handle a larger share of security and regulatory requirements.

- Fragmented reporting: Data is spread across systems unless you build your own reporting layer.

- Longer time to launch: Getting everything live takes more coordination and testing.

Payment service provider vs. payment gateway: 6 key differences

These six differences will help you understand where each option creates friction or saves effort, so you can choose the setup that fits how you want to run your payments.

1. Scope of service

The main distinction between payment service providers and payment gateways is how much of the payment flow each option actually covers.

A payment gateway handles a single step: It securely captures payment details at checkout and sends them to the next provider (e.g., a processor or acquiring bank). It’s a technical layer focused on data transfer.

A payment service provider covers the entire payment flow. It includes gateway functionality, but also handles payment processing and settlement, and often provides a merchant account.

In other words, the gateway is just one part of what a PSP already bundles together.

2. Merchant account handling

A merchant account is the account where your funds are held before payout.

With a payment gateway, you need to set up your own merchant account with an acquiring bank, as the gateway doesn’t provide it. This gives you more control, but also means more contracts, onboarding, and ongoing management.

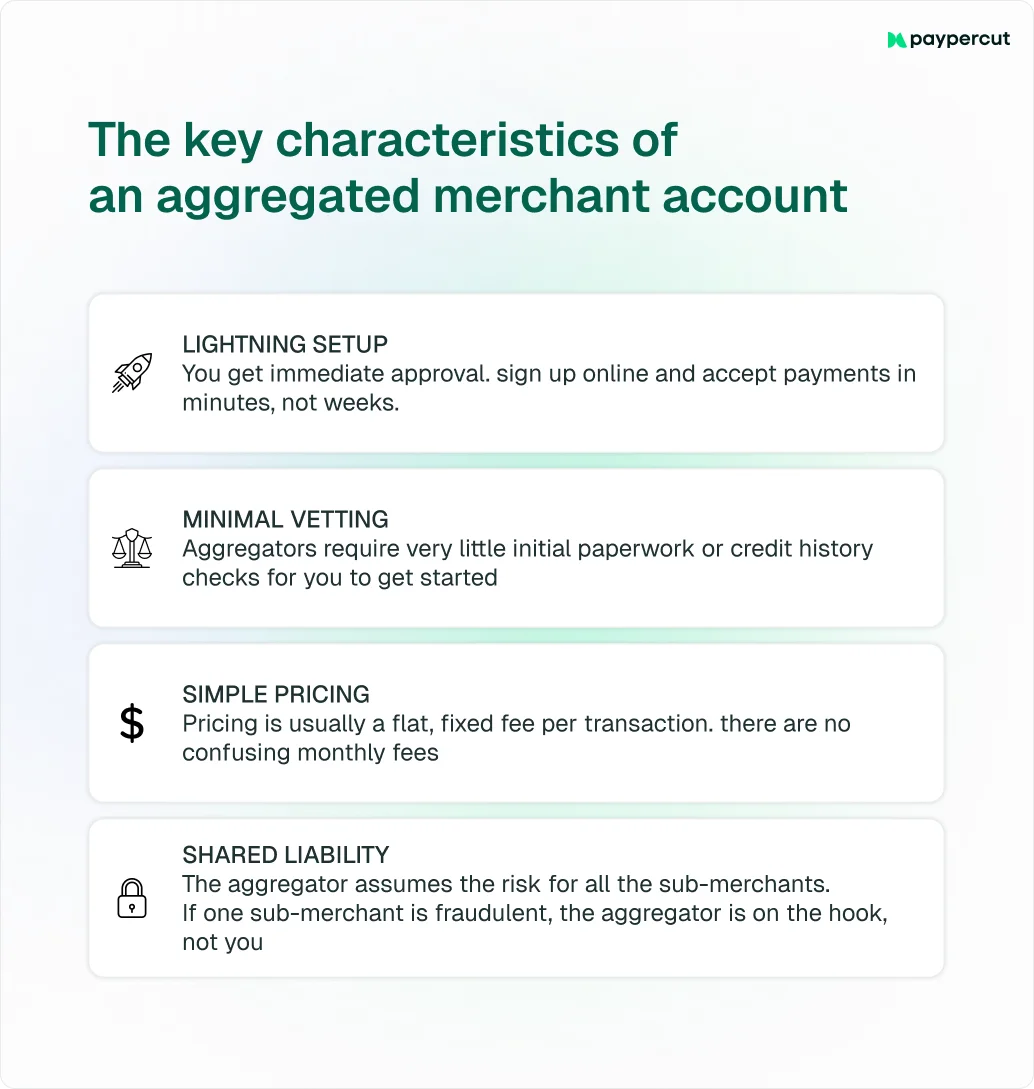

When working with a payment service provider, this is handled for you. Most PSPs provide an aggregated merchant account, so you don’t need a direct relationship with an acquiring bank. You sign one contract, and you can start accepting payments.

3. Infrastructure and setup

The difference here comes down to how much you have to build yourself.

With a payment gateway, you’re putting together your own payment infrastructure.

The gateway gives you the core connection, but you still need to integrate and manage the surrounding pieces: banking connections, fraud tools, compliance setup, and reporting.

This usually means more work for your development team and more coordination between providers.

With a payment service provider, most of that infrastructure is already in place.

You get a single integration that includes security, compliance, multiple payment methods, and a unified dashboard.

4. Settlement and funds flow

A gateway doesn’t handle the money; it only passes the transaction along.

Funds move from the customer’s bank to your merchant account via your acquiring bank.

A PSP handles this step for you.

It manages the settlement and pays out funds to your account after processing.

5. Customization and control

All the added complexity that comes with a gateway setup leads to one key advantage: You have full control over how your payments are structured.

You can choose your acquirer, negotiate fees, and decide how transactions are routed and processed.

With a PSP, that control is reduced.

Pricing, flows, and setup are mostly predefined, which makes it faster to launch but harder to tailor as you grow.

6. Pricing and cost structure

When it comes to pricing, payment service providers are easier to understand and predict, as one fee practically covers everything.

On the other hand, a gateway setup can look more complex, but it gives you room to optimize costs across providers, which starts to matter once your volumes grow.

Here’s how those pricing models differ in practice:

Payment service provider vs. payment gateway: Which setup makes more sense for your business?

Whether a payment service provider or a payment gateway makes more sense for your business depends on your business stage, payment volume, and the level of control you want over your payment flow.

When a payment service provider makes more sense

- You want to go live quickly without building a full payment setup. (e.g., a new Shopify or WooCommerce store launching in multiple markets)

- You prefer one provider instead of managing multiple partners. (e.g., a small team without dedicated payments or tech resources)

- You want to offer multiple payment methods from day one. (e.g., accepting cards, wallets, and local methods)

- You’re expanding into new countries and need local coverage fast. (e.g., entering Poland, Romania, and Hungary with local payment options)

- You want predictable pricing and simpler operations. (e.g., a growing SMB tracking margins and cash flow closely)

When a payment gateway setup makes more sense

- You already have an acquiring setup and want to build around it.

- You want to optimize fees across providers as volume grows. (e.g., processing over €1 million monthly)

- You need more control over how payments are routed and processed. (e.g., sending transactions to different acquirers by country)

- You have technical resources to manage a more complex setup. (e.g., an in-house development team handling integrations)

- You require custom payment flows or specific compliance setups. (e.g., marketplaces, platforms, or regulated industries)

Paypercut: A simpler way to run payments

The payment service provider vs. payment gateway comparison makes it clear: PSPs are easy to start with, while gateways give you more control later.

However, both options come with compromises.

That's why you might want to consider a third option—one that offers the simplicity of a PSP on the surface, with the routing flexibility of a gateway underneath, without forcing you to give up either.

That option is Paypercut, a unified payment layer built for SMBs in Europe, designed to keep payments simple without locking you into a rigid setup, especially if you're selling across multiple European markets.

It allows you to:

- Accept cards, wallets, and Buy Now, Pay Later through one integration: Offer the payment methods your customers expect without adding separate providers.

- Activate multiple BNPL providers without extra work: Give customers installment options while managing everything from one place.

- Choose how you want to integrate: Use plugins, hosted checkout, embedded checkout, or APIs.

- Collect payments even without a full checkout: Use payment links or QR codes for invoices, bookings, or quick payments.

- Sell across Europe with local payment logic built in: Currencies, payment methods, and compliance are handled per market.

- Run payments from a single dashboard: Keep track of transactions, payouts, and performance in one place.

Choosing Paypercut for handling online payments also means:

- Less operational overhead: There’s no need to manage multiple providers, contracts, or integrations.

- Faster time to market: Fully digital onboarding and ready-made integrations reduce setup time.

- Stronger checkout performance: Local methods and BNPL options help improve conversion and order value.

- Simple, predictable pricing: You are charged only transaction-based fees with no setup costs or long-term commitments.

- Support that actually helps: You receive direct access to real people who understand your setup and market.

If you want to get started, book a 30-minute consultation with the Paypercut team to go through your current setup and see what fits best, or create your account right away.

You may also like

FAQ

What is the difference between a payment service provider and a payment gateway?

The main difference between a payment service provider and a payment gateway is that the latter handles the secure transfer of payment data, while the former covers the full process, including processing, settlement, and often the merchant account.

Are payment gateways considered service providers?

No, they aren’t. A payment gateway is one part of the payment flow, while a service provider includes the gateway along with the rest of the payment infrastructure.