Installment payments reduce one of the biggest barriers at checkout: price shock.

Instead of losing customers at the moment of purchase, you give them a way to commit without paying the full amount upfront.

For you as a merchant, this means reaching more buyers without cutting your prices.

The popularity of installment payments is increasing. Europe's BNPL market grew at a 20.6% rate between 2021 and 2024, and by 2030, it’s expected to reach 293.7 billion USD. Flexible payment options are standard across most CEE e-commerce categories, and customers expect them. Merchants that don't offer them lose sales to those who do.

This guide will explain how to accept installment payments in detail. You’ll also learn how implementing this payment method can benefit your business and what challenges you may encounter.

Key takeaways

- Installment payments help you sell more without lowering prices.

Splitting purchases into smaller payments makes your products accessible to more customers and increases the average purchase value.

- Working with a third-party provider saves time and reduces risk.

Instead of building payment tracking, compliance, and collection systems yourself, you can opt for a provider that handles it all for you. Many also pay you the total price upfront.

- Transparency builds trust and reduces disputes.

Clearly communicate installment terms, schedules, fees, and penalties before purchase. Besides being required by law, this step will minimize customer complaints and chargebacks.

- The right platform removes the operational burden of installment payments.

Paypercut allows you to connect multiple BNPL providers across Europe and manage them from your dashboard. It also simplifies setup with plugins for common platforms, fully digital onboarding, and regional expert support.

How do installment payments work?

From the customer’s perspective, the experience is simple. Behind the scenes, however, several steps happen to manage risk and payment collection.

In Europe, you either manage installments yourself or work with a financial provider that handles them for you.

The process of carrying out installment payments as a merchant usually goes as follows:

- Terms agreement: The customer chooses to pay in installments at checkout and selects the schedule, such as weekly or monthly. They review your terms, including the total cost, schedule, and interest or fees, before confirming.

- Eligibility assessment: In some cases, such as fixed-payment schedules with interest, the financial provider is legally required to assess the customer’s ability to afford the loan and abide by contractual obligations.

- Initial payment: Merchants often require a down payment for high-value purchases, which may influence the installment amounts and interest.

- Automatic payments: The customer receives the purchased product or service. You charge the customer automatically according to the agreed schedule. Payments stop once the full price is covered.

Interest is common on larger purchases with longer terms—it compensates for the delayed payment and the risk that comes with it.

In addition to the original price, processing fees, and interest, the customer may also need to pay penalties for late payments or cancellations.

Installment payments and Buy Now, Pay Later (BNPL): What’s the difference?

Installment payments are the broader concept encompassing any arrangement in which the customer pays for purchases over time. How that's structured, who finances it, and who carries the risk can vary.

Buy Now, Pay Later is a type of installment payment that’s usually short-term, interest-free, and built into the checkout flow. In most cases, the customer splits the payment into three (Pay in 3) or four installments (Pay in 4) over weeks or months.

Depending on your chosen BNPL platform and model, you may receive the full payment amount upfront, with financing, eligibility approvals, and payment collection handled on your behalf. However, some platforms also let you handle the financing yourself if you need more control over the payment processes.

.avif)

Types of installment payments

Get familiar with common types of installment payment plans, though note that these are not mutually exclusive:

How to accept installment payments—Preparation, setup, and best practices

How you set up installment payments depends on whether you choose to offer them in-house or use a third-party provider.

Running them in-house gives you somewhat lower transaction fees and more control, but also significantly more work, both upfront and ongoing. You need to:

- Track every payment and reconcile manually

- Stay compliant with local consumer credit laws

- Run your own customer eligibility checks

- Absorb the cash flow risk when customers pay late or default

- Handle collections yourself when payments are missed

For most small and mid-sized businesses, these operations create a massive administrative bottleneck that detracts from their core mission.

Working with a third-party provider takes most of that off your plate. You get the installment functionality without building the infrastructure, and in many cases, you receive the full payment upfront while the provider handles the risk. Here's how to get started:

1. Choose a suitable provider

Review the locally available options and weigh them carefully against your needs.

Focus on what matters most for your business, such as fees, supported markets, setup complexity, and accepted payment methods. If you sell across multiple countries, check whether the provider works in all of them or if you'll need to piece together separate integrations.

Whatever you choose, make sure the provider:

- Meets Payment Card Industry Data Security Standards (PCI DSS)

- Follows local data protection laws, i.e., the General Data Protection Regulation (GDPR)

- Has mostly positive reviews on various platforms and forums

- Offers high-quality support that can resolve issues promptly

A BNPL aggregator like Paypercut can save you the trouble. Instead of integrating with each provider individually, you connect with Paypercut to access multiple, pre-vetted BNPL options through a single setup and dashboard, without lock-in contracts.

2. Integrate the provider into your checkout

Once you sign with a provider, the next step is to connect it with your store. Many providers offer plugins for popular platforms like WooCommerce, Shopify, and OpenCart. Plugins make implementation fast and straightforward, even for users with limited technical knowledge.

If your platform isn't supported, you'll need developer resources for the API integration—factor that into your timeline and budget.

Once the integration is ready, add the installment option to your checkout flow and update your interface accordingly.

How and where you present this option also matters. If customers only see installment options at checkout, most of the conversion impact is already lost. Show them earlier—on product pages or next to the price—so the decision feels affordable from the start.

Also, connect the system to your accounting software as soon as possible. Reconciling installment transactions manually across tools can quickly become a headache if you skip this step.

3. Specify the terms clearly

Decide which installment options make sense for your margins and order values. Set minimum thresholds if the per-transaction fees don't justify small orders. Consider whether to require down payments on higher-priced products, as they lower risk and give you cash in hand sooner.

On the checkout page, provide all the details of your installment options. Your customers should be aware of the terms, schedule, fees, interest rate, and potential penalties before making a purchase. Transparency builds trust and reduces disputes later.

Don’t forget to add the “obligation to pay” disclaimer to your “Order” button to comply with EU laws and protect your rights if a customer fails to pay.

When the purchase is final, send them the payment schedule along with the receipt or invoice.

4. Adapt your workflows

Update your internal processes to handle the new payment flow, including order management, refund procedures, and reporting.

It’s helpful to create a knowledge base article or an FAQ section to improve access to information. Train your employees to respond to inquiries, resolve problems, and thus keep customers informed and satisfied.

Make sure to update your Privacy Policy. You are legally required to disclose that you’re sharing customer data with the provider for payment purposes.

Once you're live, promote the option on product pages, in cart, and at checkout. Installments help conversion if customers know they're available.

Advantages of accepting installment payments

Installment payments benefit both you and your customers. Here’s what you can expect once you implement this method:

Increased conversions

High prices cause hesitation, even when the product justifies the cost. Splitting the total into smaller payments lowers the commitment at checkout. That “maybe later” turns into “okay, let’s do it.”

As your products become affordable to a broader range of buyers, you should see a measurable lift in conversion rates.

Higher average order value

When customers can spread the cost, they're more comfortable choosing premium items and adding extra ones to the cart. RBC Capital Markets estimates that BNPL raises ticket size by 30–50%. Another study claims that customers who use BNPL spend 6% more when shopping online.

Staying competitive

More and more businesses today offer flexible payment options. If your checkout doesn't support installment payments, customers who want them will find a competitor that does. In CEE, where installments are popular, offering them is no longer about staying ahead but rather being on a level playing field.

When installment payments might not be worth it

Installment payments are not a guaranteed win for every merchant.

If your average order value sits below €30–40, per-transaction fees may eat more margin than the conversion boost adds back.

Products with high return rates also complicate processes. Refunding an installment purchase involves more steps and longer timelines than refunding a single card payment.

And if your customer base still relies heavily on cash-on-delivery or bank transfers, adoption may be slower than expected. If you’re unsure, it’s advisable to test with a small rollout first.

Here’s a quick decision guide:

- AOV above €50 → consider BNPL or installments

- AOV below €30 → usually not worth the fees

- High return rates → be cautious (refund complexity increases)

- Cross-border → use providers, not in-house

Challenges to consider when implementing installment payments

The benefits of implementing installment payments are obvious, but you should consider the following caveats before diving in:

- Cash flow gaps: If your provider doesn't pay you upfront, you'll need to wait for the full amount while the customer pays over time. Some customers miss payments or default entirely, leaving you waiting. If you run a small business, even a few delayed payouts can create cash flow pressure.

- Complex integration: Setting up a new payment method isn’t always simple. Some providers require heavy development work, technical expertise, or lengthy onboarding processes that delay your launch. You also need to adapt your workflows and educate your employees, so be prepared to invest the time and effort.

- Cross-border complexity: If you want to offer installment payments across multiple markets, you may end up juggling separate integrations, dashboards, and agreements for each provider. Paypercut can remove this complexity with its BNPL aggregator, which allows you to easily integrate with multiple providers across borders.

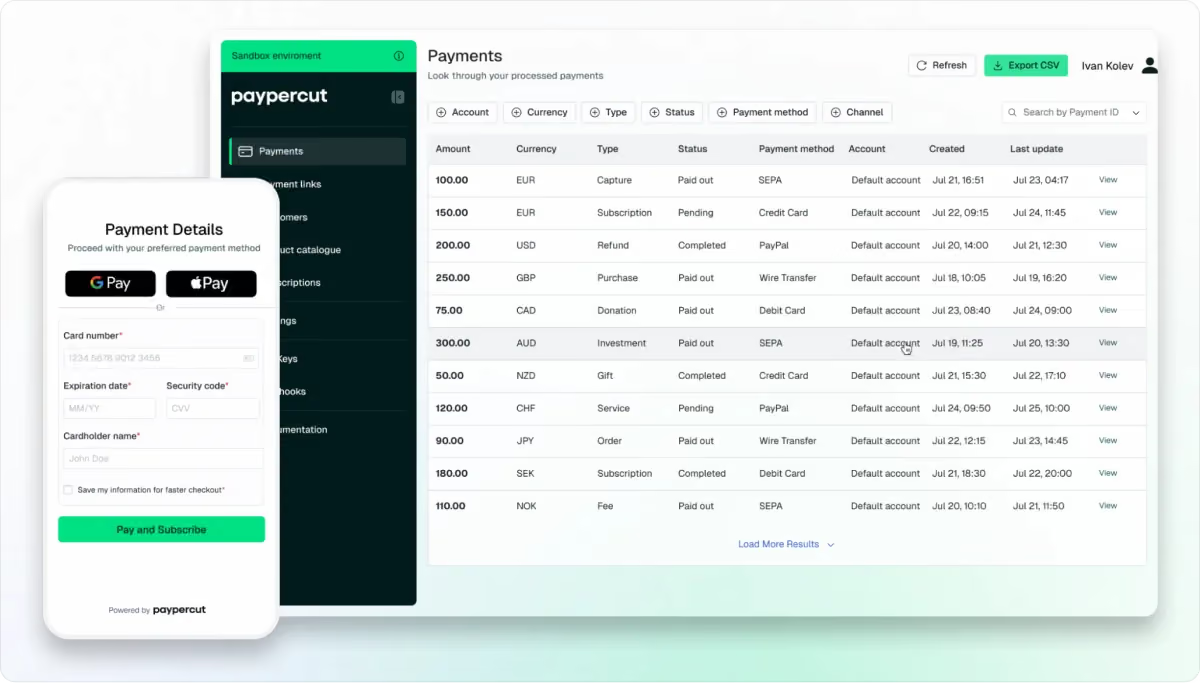

How Paypercut simplifies installment payments

Paypercut is a payment platform built for SMBs in Central and Eastern Europe. It helps merchants offer installment-based payment experiences in two ways: through third-party BNPL providers aggregated into a single integration, and through merchant-funded models where applicable.

The BNPL aggregator brings together multiple providers and presents multiple options at checkout. Here’s why this matters:

- Higher approval rates, more sales: BNPL providers reject a portion of applicants. With multiple providers competing for the same transaction, more customers get approved, and more of your sales go through.

- Upfront payouts, no cash flow drag: When a customer pays in installments, you receive the full amount immediately (minus a small transaction fee). Each provider handles collection and assumes the risk of missed payments. Your cash flow doesn't depend on whether the customer follows through.

- Simpler cross-border expansion: Paypercut is active in 29+ European countries. If you're selling cross-border, you don't need to source and integrate separate BNPL providers for each market. One setup covers multiple countries, with local currencies and compliance handled automatically.

The merchant-funded model allows you to use Paypercut's infrastructure without the upfront payouts. You take on the risk, but also get control over approval decisions and lower per-transaction costs.

With Paypercut, your business also benefits from:

- No lock-in or hidden fees: Paypercut charges per transaction, and doesn’t entail setup fees or long-term contracts.

- Fast and effortless setup: With fully digital onboarding and plugins for common platforms, you can get started within days. As for BNPL setup, Paypercut will provide you with a ready list of providers. You only need to activate or deactivate them.

- Regional expert support: If you have questions or run into problems, you’ll get help from real local experts who know your business—not bots.

If you're already seeing drop-offs on higher-value products, installment payments are one of the fastest ways to recover them—without changing your pricing.

Get started with Paypercut and add installment options to your checkout in days.