Did you know that over 57% of European consumers have already used a Buy Now, Pay Later (BNPL) service?

With this payment option giving shoppers access to items they might not have been able to afford upfront, merchants can remove financial barriers and capture demand that would otherwise be lost.

So if you’re thinking about adding BNPL as a payment option, here are the top 5 benefits of Buy Now, Pay Later to help you understand its value for your business.

Key Takeaways:

- BNPL helps boost sales and average order value

When customers can split payments into installments, they’re more likely to buy and spend more. Merchants offering BNPL see, on average, a 20% increase in total sales and reduced cart abandonment.

- Flexible payments build loyalty and attract younger shoppers

Millennials and Gen Z prefer paying over time instead of using credit cards. Offering BNPL not only appeals to these groups but also encourages repeat purchases and word-of-mouth referrals.

- BNPL reduces risk for merchants

Providers handle credit checks, installment management, and fraud prevention, giving merchants upfront payments and fewer chargebacks or disputes to manage.

- Analytics from BNPL providers unlock smarter decisions

BNPL dashboards offer insights into conversion rates, repayment trends, and customer behavior, helping merchants refine pricing, product, and marketing strategies for better performance.

- Paypercut makes BNPL integration simple and scalable

Instead of juggling multiple providers, Paypercut connects your store to several BNPL options through one easy integration. You get localized payments, flexible terms, and faster setup, all while delivering a seamless checkout experience.

What is Buy Now, Pay Later?

Buy Now, Pay Later is a payment option that allows customers to purchase products immediately and pay over time in smaller, scheduled installments.

It can be a powerful tool for you to increase sales, improve conversion rates, and attract new customers who prefer flexible payment options.

.webp)

Merchants benefit by receiving full payment upfront from the BNPL provider, while the provider takes on the repayment risk and collects installments from the customer over time.

How does Buy Now, Pay Later work?

Accepting BNPL payments is a straightforward process that integrates seamlessly into most retail platforms and checkout systems. Here’s how it typically works:

1. Sign up with a BNPL provider – You begin by creating an account with a BNPL provider. Some providers may charge a small setup or onboarding fee during registration.

2. Integrate BNPL into your online checkout – You, as a merchant, add BNPL as a payment option on your website’s checkout page, alongside existing methods like credit cards or digital wallets. This gives customers the flexibility to pay over time without leaving the store’s site.

3. Customer approval process – When a shopper selects the BNPL option, the provider performs a quick soft credit check to confirm eligibility and help prevent fraud. This typically takes only a few seconds and does not affect the customer’s credit score.

4. Customer completes the purchase – Once approved, the customer is redirected back to your checkout page to confirm order details, such as shipping information, and finalize the transaction.

5. You receive the payment – After checkout, you receive the full transaction amount upfront from the BNPL provider. Depending on the provider’s terms, there may be a brief delay before the funds are deposited.

6. BNPL provider manages repayments – The BNPL provider takes over from there, managing the customer’s installment payments and handling any missed or late payments directly.

5 Benefits of Buy Now, Pay Later for merchants

Offering BNPL options can provide significant advantages for merchants beyond simply increasing payment flexibility for customers. Here are some of the key benefits:

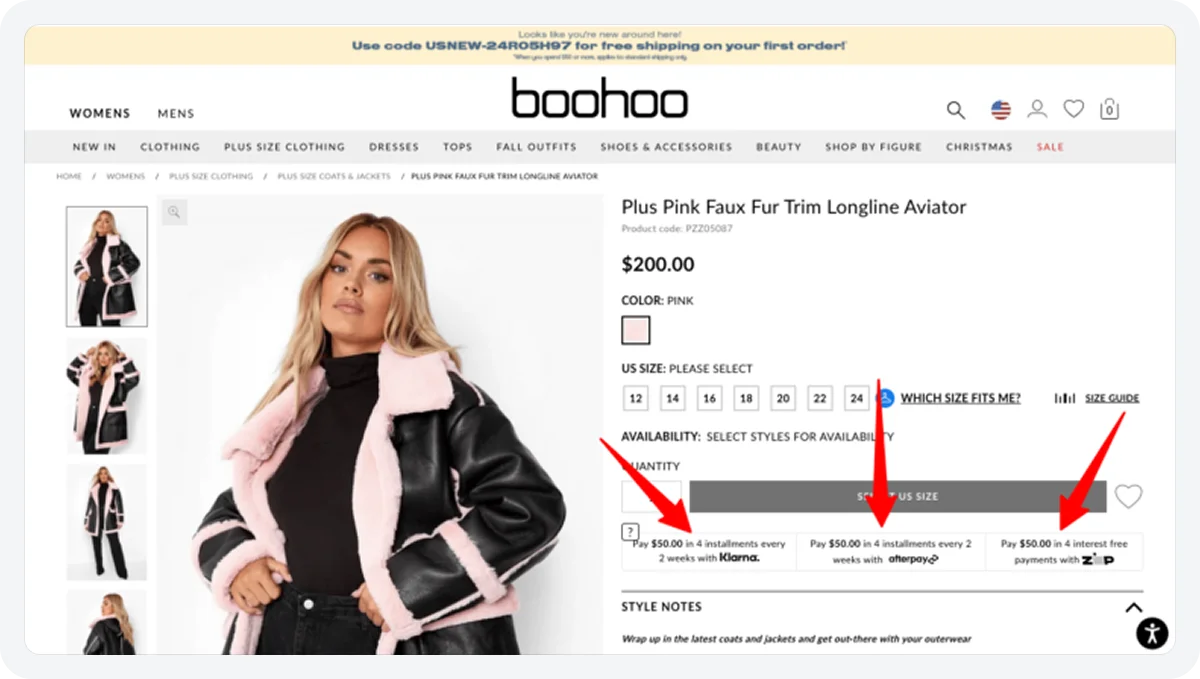

1. Increased sales and average order value

When shoppers can spread out their payments, they’re more likely to finish their purchase, especially for higher-priced items that might feel too expensive

This added flexibility not only reduces cart abandonment but also encourages customers to spend more overall.

In fact, merchants that offer BNPL options experience, on average, a 20% to 30% increase in total sales.

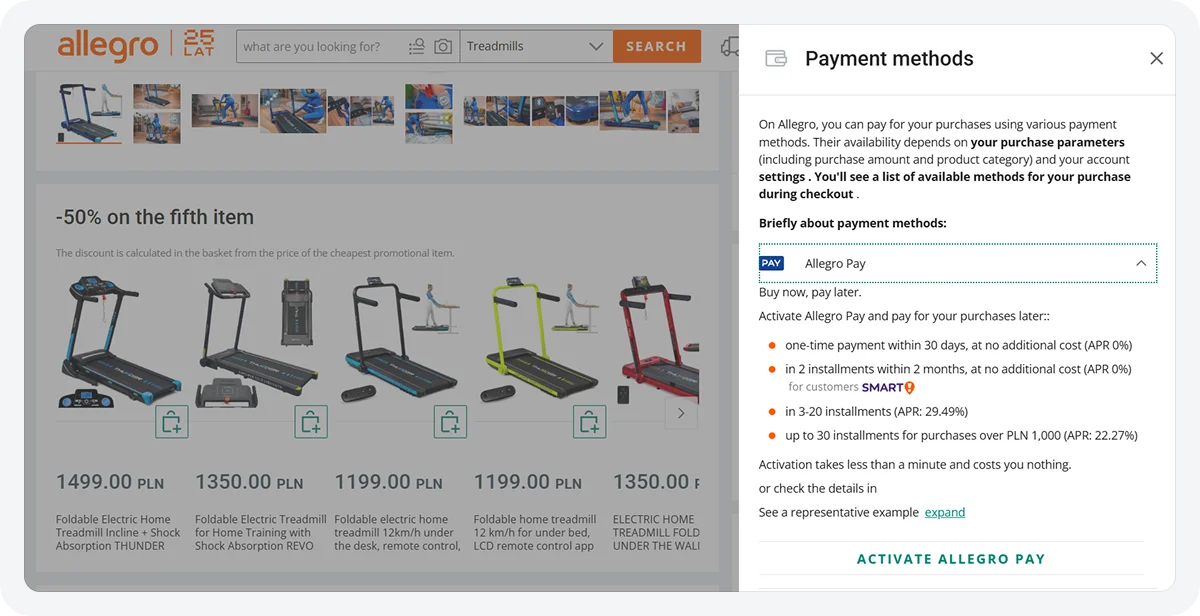

💡 Example: Allegro

Allegro, the largest online marketplace in Central and Eastern Europe, set out to make shopping more flexible and improve purchase completion rates.

By 2024, its “buy now, pay later” service, Allegro Pay, had served more than 2.2 million users, issuing PLN 10.8 billion in loans and driving PLN 16.5 billion in gross merchandise value (GMV).

To assess its impact, Allegro ran internal control tests comparing customers who had access to BNPL with those who did not. The results showed that BNPL users generated roughly 35% more GMV than the control group.

2. Customer loyalty

Flexible payment options also help you build stronger, longer-lasting relationships with your customers. Shoppers who know they can pay in a way that suits their budget are more likely to return for future purchases and recommend your business to others.

Offering BNPL can also set you apart from competitors. When customers compare similar products on two websites, a flexible payment option might be the deciding factor that wins you the sale and their loyalty.

💡 Tips for strengthening customer loyalty with BNPL

- Promote BNPL as a customer benefit – Position it as a convenience, not just a payment method. Highlight how it makes shopping easier and more flexible for your customers.

- Show BNPL early in the shopping journey – Display BNPL messaging on product pages and ads so customers know right away that flexible payment options are available.

- Re-engage BNPL users with personalized follow-ups – Send tailored reminders or offers to encourage repeat purchases and keep your brand top of mind.

- Integrate BNPL with your loyalty program – Allow customers using BNPL to earn points or rewards, reinforcing that every purchase, no matter how it’s paid for, brings extra value.

3. Appeal to younger shoppers

Younger shoppers, in particular millennials and Gen Z, are embracing “Buy Now, Pay Later” in large numbers.

Since younger consumers tend to shop online more, have less savings, and are less likely to use credit cards, offering flexible payment options helps you reach this valuable group and makes them more likely to choose your brand.

💡 Example: PayPo (Poland)

PayPo, Poland’s leading “Buy Now, Pay Later” platform, is especially popular among younger, mobile-first shoppers.

A 2023 CASE Research Institute report found that 75% of BNPL users in Poland are under 44 years old, and 64% do not have a credit card.

Industry data also show that BNPL is most often used for fashion and electronics purchases, which are particularly popular with younger online consumers.

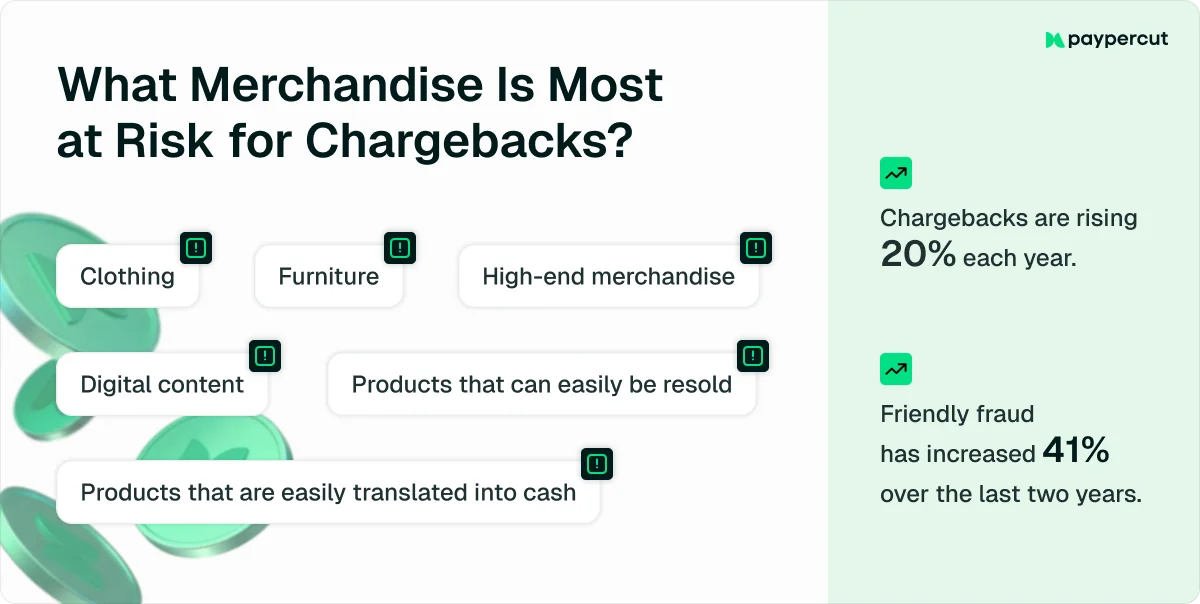

4. Reduced risk of chargebacks and fraud

Partnering with a BNPL provider helps protect your business from costly chargebacks and fraudulent activity.

Since your BNPL partner manages the financing, payment processing, and credit checks, they often assume the credit and fraud risk for each transaction so that you can focus on sales instead of disputes.

By shifting this responsibility to your BNPL provider, you gain peace of mind knowing that transactions are being screened, verified, and securely processed behind the scenes.

That said, it’s still important to make sure you’re working with a trusted and secure provider. Before you choose one, make sure to:

- Review independent reports and reviews – Look for performance data, security certifications, and customer feedback about the provider’s reliability and fraud prevention.

- Assess their fraud prevention technology – Ensure they use advanced risk assessment tools, encryption, and real-time fraud detection.

- Check regulatory compliance – Verify that your provider complies with local and EU financial regulations and data protection standards.

5. Better conversion analytics & insights

Most BNPL providers offer comprehensive dashboards and real-time analytics that can give you valuable insights into customer purchasing behavior, including metrics such as average order value (AOV), repayment trends, and conversion rates.

These insights help you:

- Identify which products perform best among BNPL users.

- Understand customer lifetime value (LTV) and repeat purchase behavior.

- Refine marketing strategies and optimize checkout experiences for higher conversions.

A strong BNPL provider should give you actionable insights across key performance areas:

What merchants should keep in mind when offering BNPL

While BNPL programs can boost sales and attract new customers, it’s important, especially for small or growing businesses, to look beyond the advantages to understand the potential downsides and how to address them.

You should keep an eye on:

1. Transaction fees

BNPL providers charge merchants a fee for every transaction, typically 3% to 6%, which is higher than standard credit card processing fees.

- For low-margin businesses, these higher fees can significantly reduce profitability.

- Over time, even small differences in transaction costs can make a big impact on your bottom line.

💡 How to manage it

- Compare providers carefully: Look at fee structures, settlement times, and terms before choosing a BNPL partner.

- Negotiate rates: Many providers are open to customized pricing if your transaction volume is high or growing.

- Set minimum purchase thresholds: Apply BNPL only for orders above a certain value to ensure fees are worth it.

- Factor fees into pricing: Slightly adjust your product prices or shipping fees to offset the additional cost.

2. Higher return rates from impulse buys

BNPL makes it easy for customers to click “Buy” without much hesitation, which can also lead to more returns. Every return affects your profit margins, especially since BNPL fees are typically non-refundable once a transaction is processed.

💡 How to manage it

- Highlight return policies clearly: Ensure customers understand your return terms before they buy.

- Encourage thoughtful purchasing: Use features like “save for later” or detailed product info to reduce impulsive decisions.

- Track return data: Identify which products or promotions drive the most BNPL returns and adjust your strategy accordingly.

- Build in safeguards: Consider offering BNPL only for products with low return rates or higher profit margins.

3. Integration and operational challenges

Adding BNPL to your checkout isn’t always a quick or straightforward process. Depending on your eCommerce platform, payment gateway, and internal systems, you may encounter technical snags, reconciliation issues, or fulfillment slowdowns that take time to iron out.

💡 How to manage it

- Test before going live: Pilot BNPL on a small product range or limited audience to identify checkout glitches, tracking gaps, or processing delays before full rollout.

- Work closely with your provider: Clarify how refunds, chargebacks, and payouts are managed so your finance and support teams can respond quickly when issues arise.

- Align BNPL with your existing systems: Make sure your BNPL data flows smoothly into your inventory, accounting, and CRM tools to keep records accurate and minimize manual work.

- Gather customer feedback: During the first few months, listen closely to what shoppers say about their BNPL experience, small usability fixes can prevent larger checkout problems later.

Access multiple BNPL providers through one platform

While setting up Buy Now, Pay Later options can be a smart move for any merchant, maintaining multiple providers and integrations across regions often adds unnecessary complexity.

What starts as a simple way to boost sales can quickly turn into a maze of contracts, plugins, and fees that drain time and focus.

That’s where Paypercut comes in.

As the first BNPL aggregator in Central and Eastern Europe, Paypercut lets you offer cards, digital wallets, and BNPL through a single integration.

It connects your store to multiple local and global providers at once, simplifies settlements, and helps you scale effortlessly across borders

How can Paypercut help you:

🟢 One integration, multiple BNPL options – Connect to several BNPL providers instantly through a single API or plugin, improving acceptance rates and flexibility for customers.

🟢 Localized payments and settlements – Operate seamlessly across Bulgaria, Greece, Romania, Czechia, and beyond, with local currency settlements to reduce FX risk.

🟢 Zero lock-in, pay-as-you-go model – No setup fees or contracts, you only pay a small percentage per transaction.

🟢 Merchant-funded BNPL options – Offer installments even in markets without local providers, while maintaining full control over risk and approval.

🟢 Partner revenue opportunities – Earn revenue by onboarding other merchants through Paypercut’s partnership program.

🟢 Flexible payment options – Accept card payments, Apple Pay, Google Pay, recurring billing, and BNPL, all in one platform.

🟢 Human support and simple setup – Get personal onboarding assistance, intuitive dashboards, and plugins for WooCommerce, OpenCart, and Shopify.

Sign up today and discover how Paypercut can help you offer smarter, more flexible payments that drive sales and simplify your checkout experience.