In 2026, the European payments market is expected to process around €0.64 trillion, and analysts estimate it could reach €1.27 trillion by 2031. That’s nearly 15% annual growth.

The momentum is strong across the region, including Central and Eastern Europe (CEE), where digital payments are expanding quickly as more businesses sell online and customers move away from cash.

But this growth isn’t driven by flashy new inventions.

Most of the changes shaping the payments market today build on existing infrastructure—things like instant payment rails, digital wallets, and embedded checkout flows. What’s changing now is how widely these technologies are used and how they’re governed.

In many ways, the industry is moving from innovation to maturity. Payments are becoming more regulated, more reliable, and more deeply integrated into everyday business tools and platforms.

For businesses, this means new opportunities, but also new expectations around speed, security, and flexibility.

With that in mind, let’s look at the top eight payment market trends in Europe in 2026 and what they mean for businesses across the region.

Key takeaways

- Instant payments are becoming the new normal

EU regulation and customer expectations are pushing banks to support instant transfers. For businesses, this means faster settlements, better cash flow, and customers who expect payments to move in seconds. - More competition in payments means more checkout options

PSD3 and open banking rules will allow more fintech providers to compete with banks. Merchants will gain access to more payment solutions and easier integrations. - Customers increasingly prefer wallets and flexible payments

Digital wallets speed up checkout and reduce abandoned carts, while BNPL helps customers spread costs and often increases basket sizes. - Payments are moving inside apps and platforms

More businesses now embed payments directly into their websites, marketplaces, or software tools. This reduces friction and improves checkout completion. - A unified payment setup makes growth easier

Platforms like Paypercut help merchants manage cards, wallets, BNPL, and cross-border payments through one integration, making it easier to offer the payment methods customers expect.

1. Instant payments are becoming the new standard

Instant payments allow money to move between bank accounts in seconds, 24/7, even at night or on weekends. Across Europe, they’re quickly becoming the expected way to send and receive money.

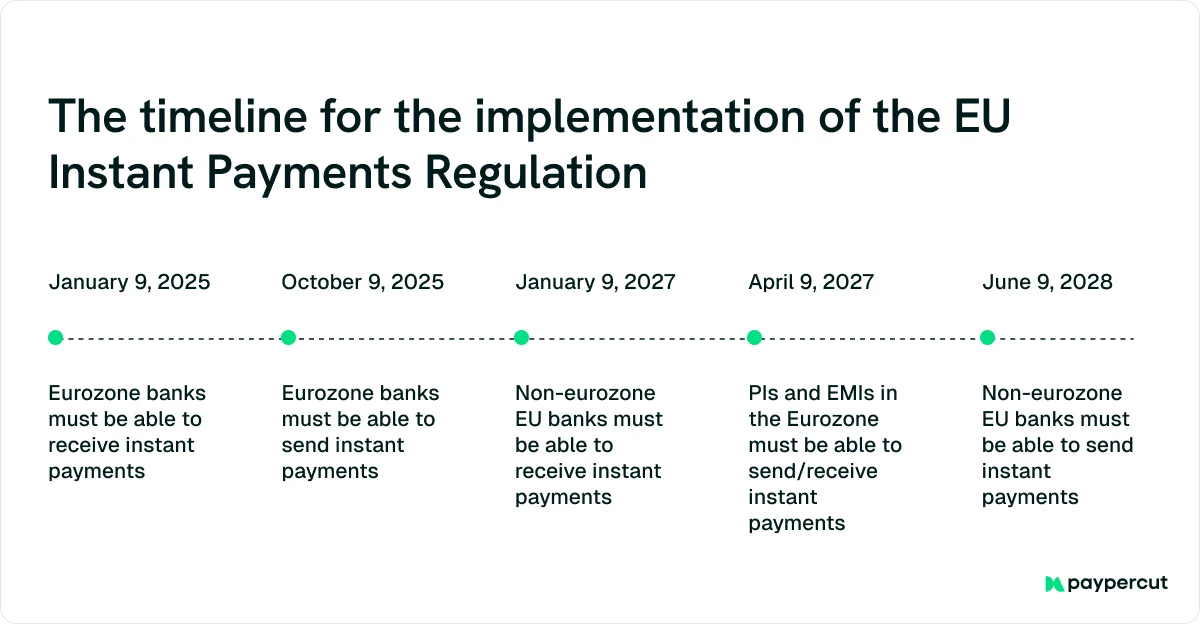

This shift is largely driven by the European Union Instant Payments Regulation (IPR), adopted in 2024, which requires banks that offer regular euro transfers to also support instant transfers at the same price.

Although the regulation was officially adopted in 2024, the first major milestones came in 2025:

- January 2025: Banks in the eurozone must be able to receive instant payments.

- October 2025: Banks must also be able to send them.

That makes 2026 the first year when instant payments truly start becoming standard across Europe.

But even without regulation, the benefits of instant transfers are clear: faster settlements, better cash flow for businesses, and a smoother customer experience.

That’s probably why instant payment systems keep expanding across Europe and CEE in particular:

- The Czech Republic: In December 2025, instant payments averaged 2.03 million per day and reached 43% of all interbank credit transfers.

- Hungary: Approximately 42% of all household bank accounts were used to initiate at least one instant credit transfer during the year.

- Romania: The RoPay instant payment network is expanding quickly, with banks like Vista Bank, UniCredit Bank, and Raiffeisen Bank launching instant transfers via QR codes or phone numbers directly in mobile banking apps.

- Poland: BLIK has become one of Europe’s clearest examples of instant-payments behavior at scale, with 2.9 billion transactions worth €104.9 billion in 2025.

2. PSD3 is opening the payments market to more competition

The Third Payment Services Directive (PSD3) is the next update of Europe’s main payments law, replacing and improving parts of PSD2.

Together with the PSR, it aims to make payments safer, more transparent, and more competitive across the EU.

The rules focus on closing gaps in the current system and making sure banks and fintech payment providers compete on equal terms.

Key changes include:

- Stronger fraud protection, including verification that the recipient’s name matches the account

- Clearer information about fees before a payment is made

- Better access to bank account data for licensed third-party providers (open banking)

- Fairer access to payment infrastructure for fintechs

The package reached a political agreement in late 2025. During 2026, banks and payment providers across Europe are preparing for the new rules before they formally enter into force.

Once they do, merchants will have access to more payment providers and checkout options, as well as an easier integration of new payment solutions through open banking.

3. Phones are turning into everyday payment wallets

More and more customers now pay directly from their phones.

Digital wallets like Apple Pay, Google Pay, and local app store card details securely and allow customers to confirm payments with a fingerprint or face scan.

The result is a faster checkout, fewer steps, and fewer abandoned carts.

This shift makes sense in a mobile-first world.

Customers already use their phones for shopping, banking, and proving identity, so paying from the same device is the natural next step.

It’s no surprise, then, that digital wallets and account-to-account payment rails are the fastest-growing payment methods in Europe, expanding at 17.74% annually.

A good example is Poland, often seen as one of Europe’s most advanced payments markets, where as many as 45% of Poles already consider digital wallets their preferred way to pay, and adoption keeps growing.

The trend isn’t slowing down globally, either.

By 2027, digital wallets are expected to account for 61% of total e-commerce transaction value, making them the dominant way people pay online.

For merchants, this means including digital wallets at checkout is quickly becoming a must.

Pro tip:

Variety at checkout matters.

While digital wallets are important, the best approach is to offer them alongside other popular payment methods, as different customers prefer different ways to pay.

The easier it is for them to use their favorite option, the more likely they are to complete the purchase.

A payment aggregator like Paypercut allows you to offer multiple payment methods through one simple integration—including cards, digital wallets, Buy Now, Pay Later (BNPL), payment links, and split payouts—so you can create a smoother checkout without managing several providers.

4. AI is starting to run more of the payments process

Artificial intelligence (AI) is no longer used just for chatbots or basic automation. In payments, it’s starting to handle bigger parts of the process on its own, including:

- Fraud detection

- Transaction monitoring

- Real-time risk scoring

- Credit scoring

- AML (Anti-Money Laundering) checks

This level of AI involvement brings tangible benefits.

AI can help payment providers react faster, reduce false declines, and catch fraud patterns that fixed rules might miss.

This is incredibly important as fraud is becoming more complex and more costly.

According to the European Banking Authority (EBA) and the European Central Bank (ECB), payment fraud in the European Economic Area (EEA) reached €4.2 billion in 2024.

But as AI starts making more decisions in payments, rules become more important.

This is where the EU AI Act comes in, treating many financial AI systems—including those used for fraud detection, transaction monitoring, and credit scoring—as “high-risk” systems.

So, as of August 2026, these systems will have to demonstrate:

- How the AI reaches its decision

- How bias or unfair outcomes are reduced

- How decisions can be reviewed, audited, or challenged

For payment providers, this means AI can still improve fraud detection and payment approvals, but the systems behind those decisions must now be transparent and accountable.

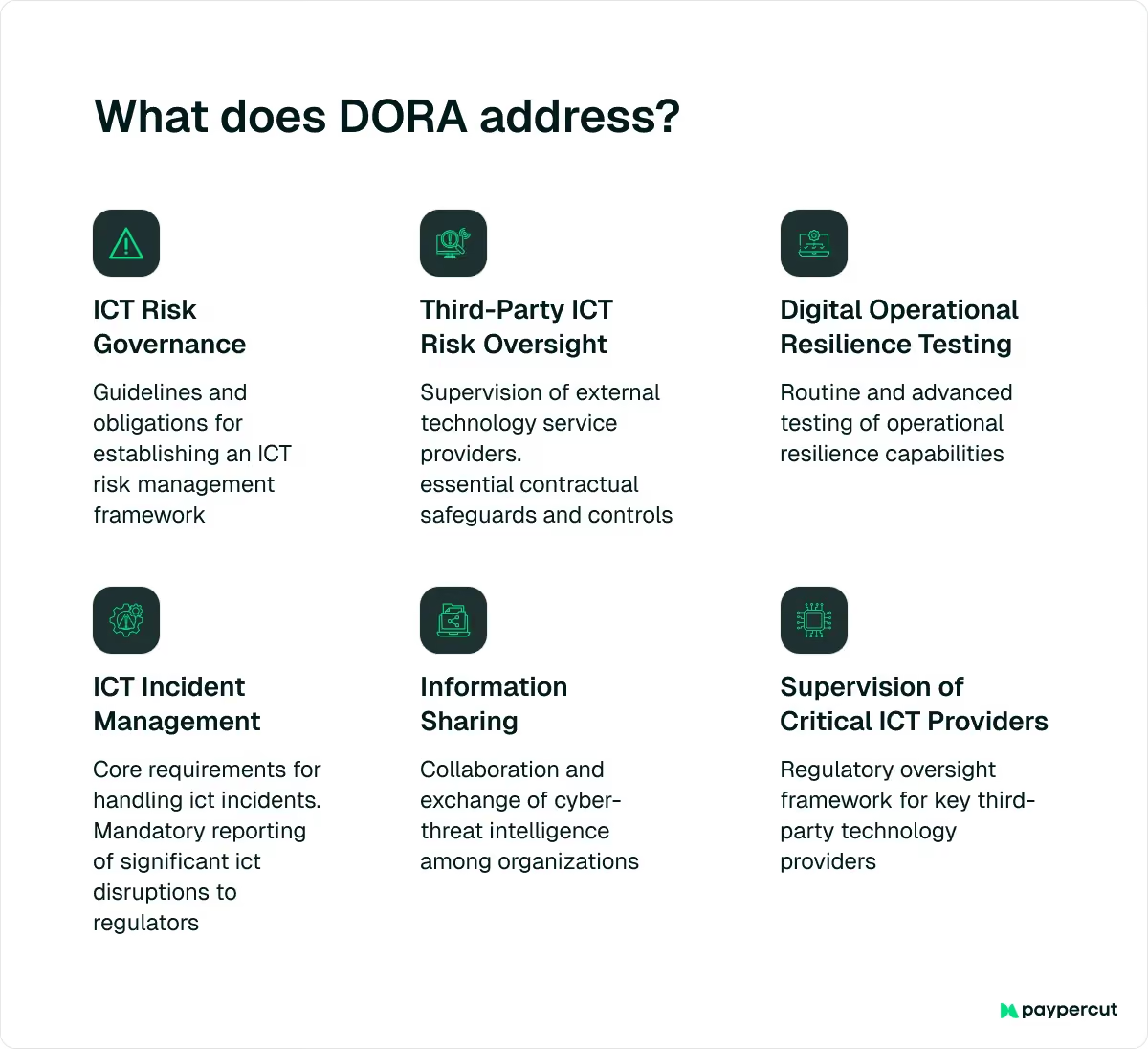

5. Payment systems now have to be more resilient

Payments rely on complex technology. If systems fail because of cyberattacks, IT outages, or issues with cloud providers, businesses may not be able to process transactions.

To address this, the EU introduced DORA (Digital Operational Resilience Act).

The regulation applies to over 20,000 financial companies, including banks, payment institutions, and fintechs, as well as major technology providers.

Its goal is to ensure that financial services can continue operating even during technical disruptions.

Although DORA entered into force in 2025, 2026 marks the start of stricter supervision and enforcement, with regulators expecting stronger risk management and oversight of technology providers.

6. Payments are being built directly into business platforms

Across Europe, payments are no longer always handled by a separate checkout page or payment app. Increasingly, they’re built directly into the platforms businesses already use, from marketplaces and delivery apps to SaaS tools and logistics systems.

For merchants, embedded payments bring several advantages:

- Fewer steps to checkout: Removing redirects and extra forms makes the payment process faster and simpler.

- Higher checkout completion: When paying is quick and easy, fewer customers abandon their purchase.

- Stronger brand experience: Businesses can design the payment flow so it matches their brand and customer journey.

- Better workflow integration: Payments connect directly with the tools businesses already use, such as marketplaces, booking platforms, or business software.

With these benefits in mind, it’s no surprise that the embedded finance market in Europe grew at a CAGR of 15.5% between 2021 and 2025, and analysts expect it to keep expanding in the coming years.

The market is projected to grow from about €110.8 billion in 2024 to roughly €167.27 billion by 2030, as more platforms integrate payments directly into their services.

Pro tip:

Embedded checkout is becoming common across many platforms, but it’s especially useful for e-commerce stores, subscription platforms, digital services, and higher-volume merchants, where fast and seamless payments matter most.

If you own one of these, you can add an embedded checkout to your website with Paypercut, which guarantees:

- Fully responsive checkout, optimized for mobile shoppers

- Easy design integration, so it matches your website without advanced coding

- Real-time field validation, reducing mistakes and failed payment attempts

7. Cross-border payments are getting faster and simpler

For a long time, sending money across borders was slow, expensive, and hard to track. Today, several global initiatives are working to modernize these payments.

One of the biggest efforts comes from the G20 Roadmap for Cross-Border Payments, launched in 2020 and coordinated by the Financial Stability Board together with central banks and international regulators.

Its goal is to make cross-border payments faster, cheaper, more transparent, and more accessible.

The roadmap sets global targets for 2027 and focuses on removing the main frictions in international payments.

This includes improving data standards, increasing interoperability between payment systems, and creating a more level playing field between banks and fintech payment providers.

At the same time, Europe is modernizing its own infrastructure.

The table below shows some of the key initiatives driving this change:

8. BNPL is becoming a powerful checkout tool

BNPL lets customers split a purchase into several smaller payments instead of paying the full amount upfront. For merchants, this often leads to higher conversions and larger basket sizes, especially in e-commerce.

The logic is simple: When customers can spread the cost over time, they’re often more comfortable adding extra items to their cart. Studies show BNPL can increase average order values by up to 40%, and some merchants report even larger gains.

Customers don’t seem to mind the higher spending either.

The European BNPL market has grown rapidly, expanding at a 25.5% CAGR between 2022 and 2025. Analysts expect the trend to continue, with the market projected to grow at 15.4% annually between 2026 and 2031, reaching about €381.91 billion by 2031.

Pro tip:

Given the numbers behind BNPL growth and its impact on basket size, adding this payment method to your checkout is a no-brainer.

What many businesses don’t realize is that you don’t have to choose just one provider. With Paypercut’s BNPL aggregator—the first of its kind in CEE—you can offer multiple BNPL options through a single integration.

During checkout, customers enter their details and receive real-time installment offers from available providers, then select the one that suits them best.

As a merchant, you receive the full payment upfront, while BNPL providers manage installments and credit risk.

As for your customers, they will see only the BNPL providers available in their country, thanks to Paypercut’s localized checkout experience.

What these payment market trends in Europe mean for your business

Payments in Europe are entering a new phase.

Instant transfers, digital wallets, embedded checkout, AI-driven risk management, and new regulations are all pushing the industry in the same direction: payments are becoming faster, smarter, and more integrated into everyday business tools.

For merchants, the opportunity is clear.

Businesses that offer flexible payment options, smooth checkout experiences, and reliable payment infrastructure will have a strong advantage in winning and keeping customers.

Paypercut takes the complexity out of managing modern payments by offering businesses:

- Multi-currency payments and fast payouts, so you can sell across Europe and beyond

- No setup fees or lock-in contracts, with simple pay-per-transaction pricing

- A self-serve portal, where you can track transactions and manage payments easily

- Human-first support, so you always have someone to help when you need it

- Fast, fully digital onboarding, allowing you to go live in hours without heavy development work

Sign up now to experience this practical onboarding or schedule a 30-minute consultation with our team to learn how Paypercut can help you stay on top of payment trends and grow your cross-border business.